Note: This was first published to subscribers yesterday.

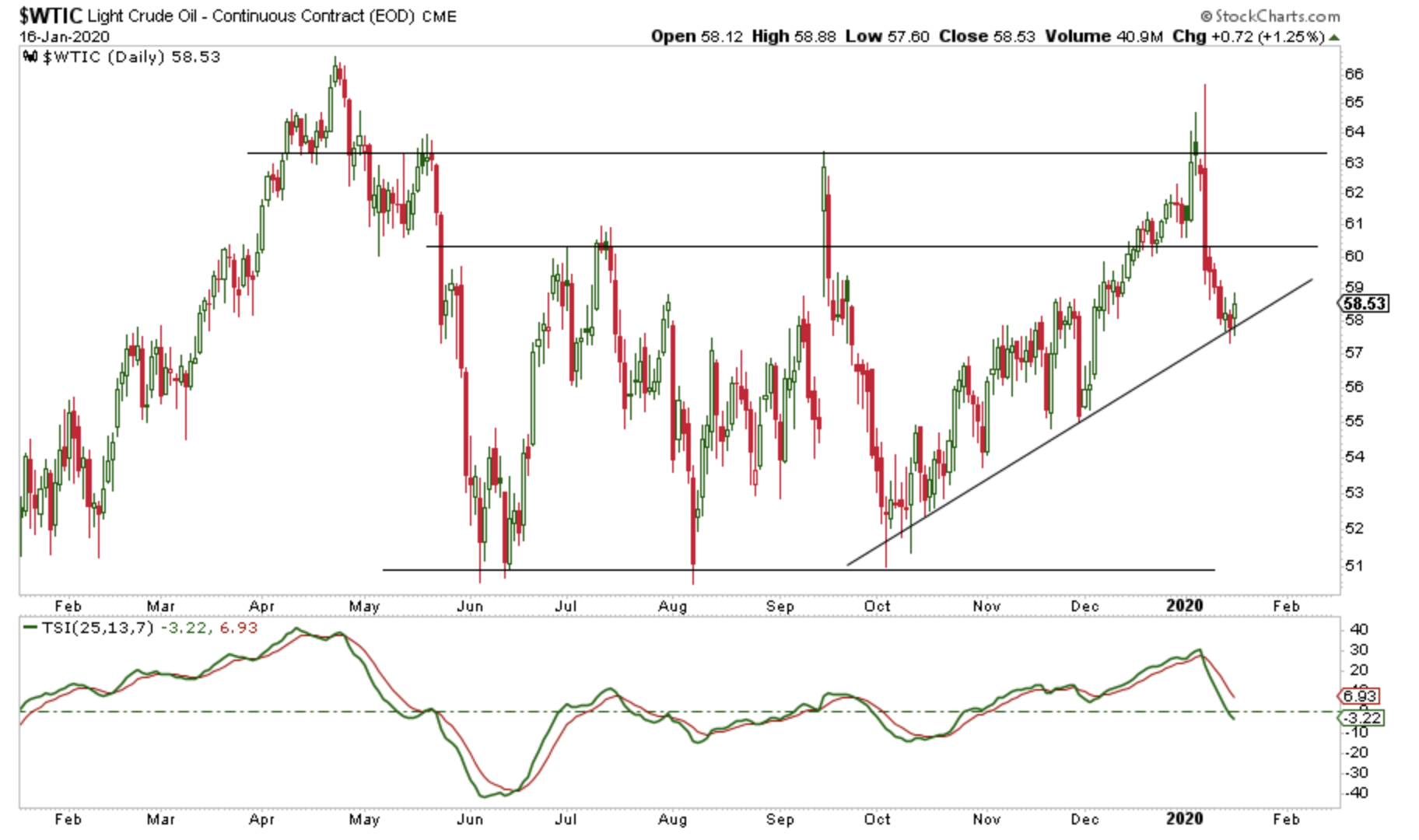

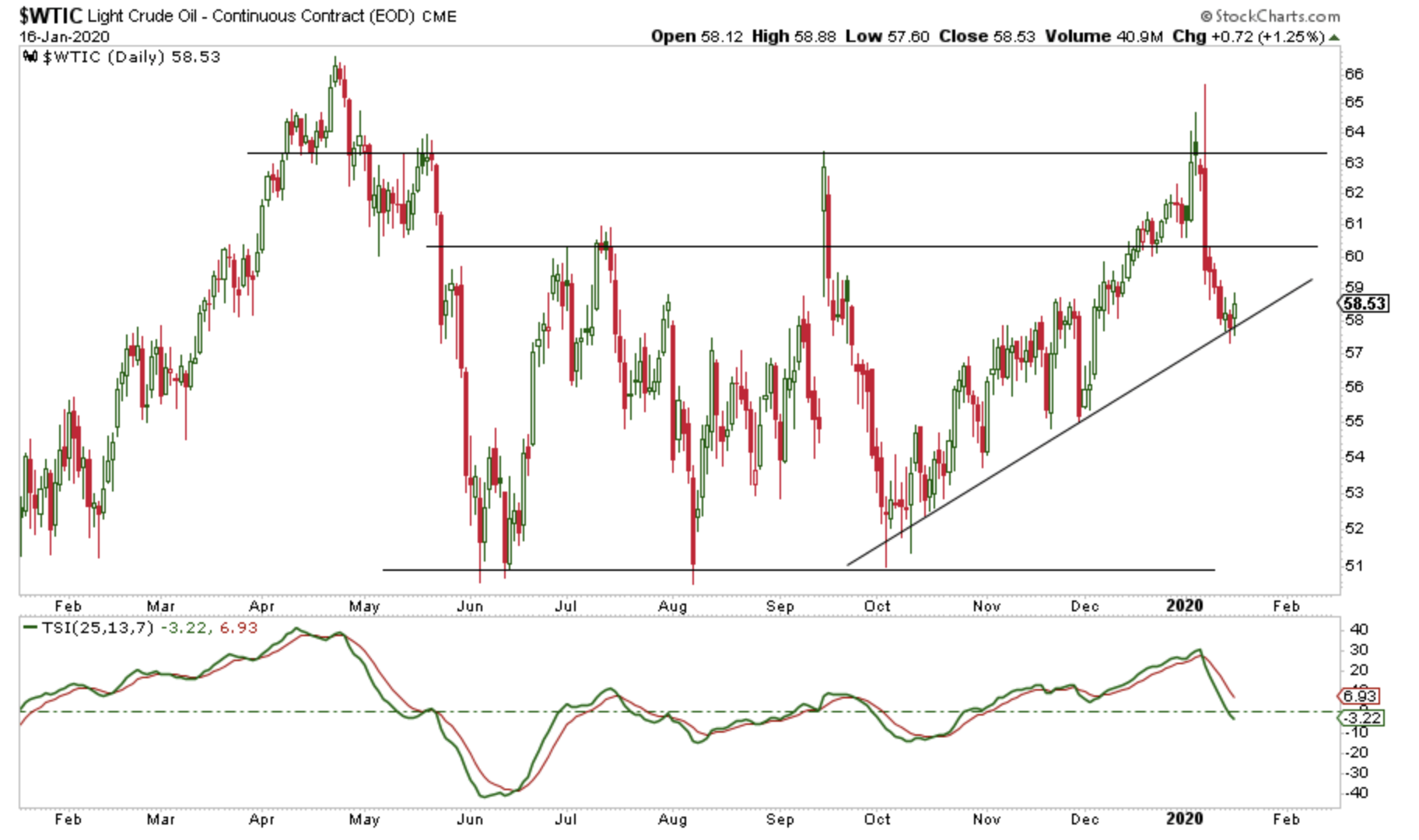

Despite headlines out of IEA today that the global oil market will be +800k b/d oversupplied in H1 2020, WTI and Brent rallied with WTI holding the crucial support at the 200-day and the up trendline.

This technical rebound combined with the latest US crude storage projections lead us to believe that WTI is likely to retest ~$60 in the next week or two. Depending on the price action during that retest, we can probably gauge our next trade set up there.

Source: EIA, HFI Research

In yesterday’s EIA oil storage report, refinery throughput for the first time in literally half a year came in well above our estimate. In fact, it was so much higher than our estimate that we now have a small draw forecasted for January balances.

We said toward the end of last year that we have automated this process, so refinery throughput is one of them. What we are basically doing is taking the lower of the two figures (monthly projected maintenance throughput or the change in five-year average throughput). Our current estimate for January is ~16.5 mb/d of throughput, so this is actually lower than what we had from the maintenance schedule.

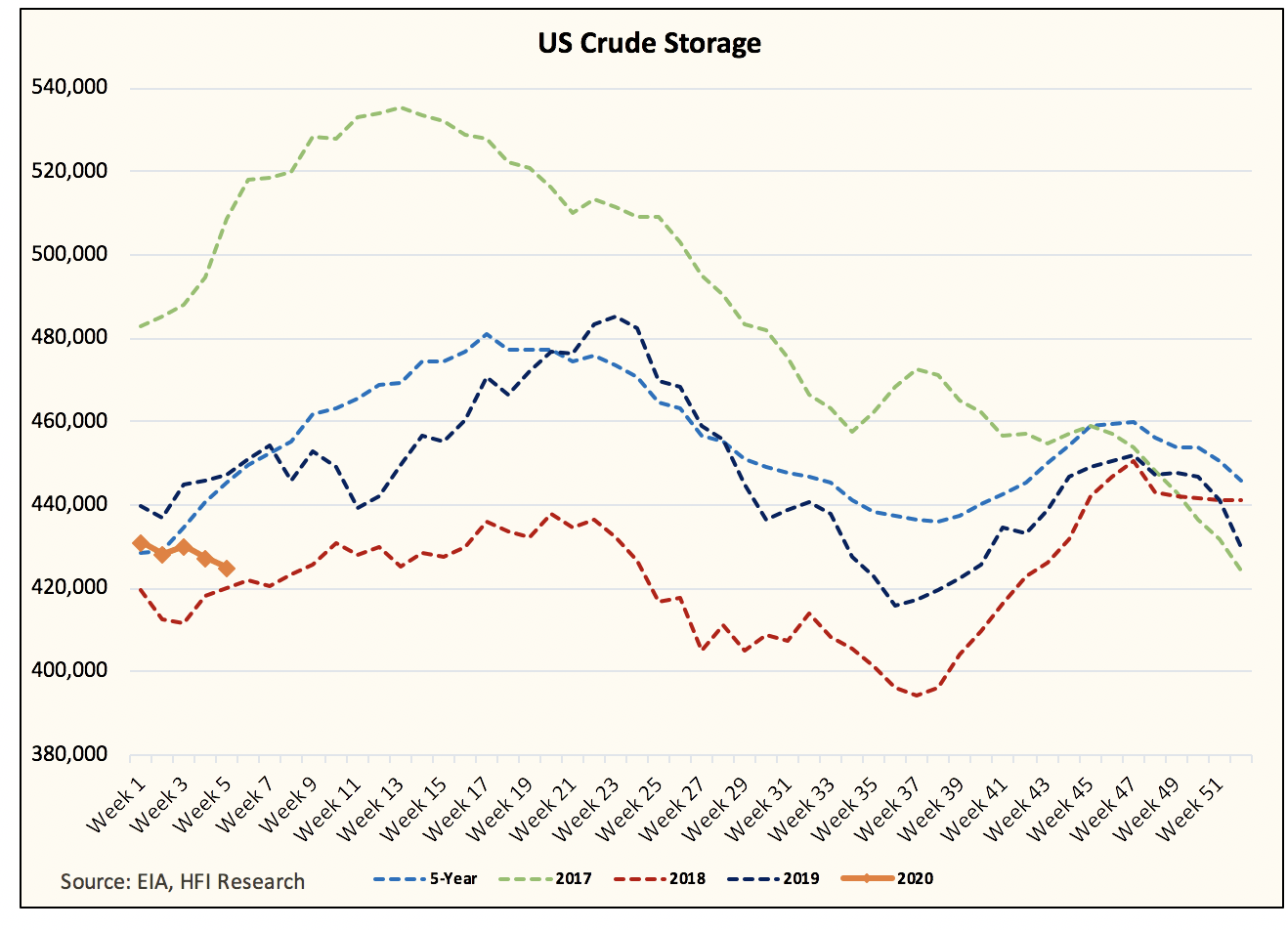

In addition, the physical oil market appears to be confirming the reversal in crude.

Brent timespreads notched another leg higher today following yesterday’s surprising reversal, and Genscape reported this morning that Cushing inventories declined ~1.1 mbbls from last Friday to this Tuesday, sending WTI timespreads from contango to backwardation.

The gist of what we are seeing at least is that products are the ones currently in oversupply, and despite reduced throughput globally, crude remains tight. Again, we have to thank a large part of that from Saudi tanking exports in January.

For the first 15 days of January, Saudi Arabia exported ~6 mb/d. This is on pace to finish the month at around ~6.3 mb/d or similar to December.

The drop would mark a ~1 mb/d decrease in crude exports year-over-year, likely explaining why the crude market is so obviously tight, while the rest of the market is not so given the seasonal decline in Q1.

All in all, the trend to keep watching for next week is whether or not EIA’s oil demand proxy rebounds. If so, product storage should display a positive surprise. Crude storage also is likely to trend lower even if refinery throughput is reduced from here.

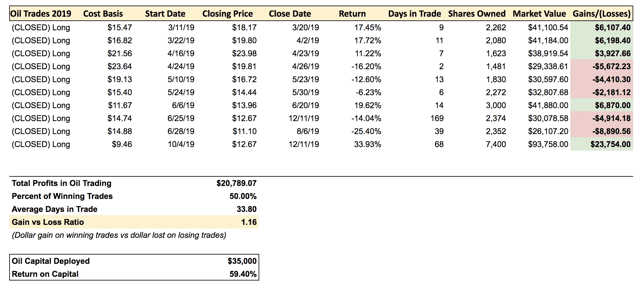

Thank you for reading this article. We launched our oil trading portfolio in 2019. The oil trading portfolio is designed to take advantage of short-term long/short oil trades in the market. For readers interested in our positioning along with real-time trades, we are now offering a 2-week free trial. Here’s our trading result from 2019:

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}