With Goldman Sachs (GS) holding its first-ever investor day less than a week from now, I have GS on catalyst watch – the new management team will likely lay out a credible path toward generating higher returns, further strengthening investor confidence going forward. With GS trading at a very reasonable ~1.1x tangible book, the potential for a higher return target within the 12-15% range leaves the risk/reward skewed firmly to the upside.

A Closer Look at 4Q Results

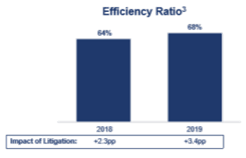

Earnings: GS reported net earnings of $1.9 billion for 4Q19, resulting in EPS of $4.69 and ROE of 8.7%. Earnings were marred by a $1.09 billion litigation charge associated with the 1MDB scandal, which burdened EPS and ROE by $2.95 and 5.3%, respectively.

Source: Company Presentation

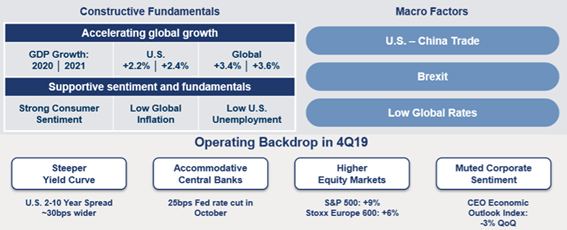

Operating Metrics: The operating environment remains constructive, with solid and measured client engagement, steadily rising asset prices, improvement in the secured funding markets, progress toward Brexit resolution, and improvements in the US-China trade tensions.

Source: Company Presentation

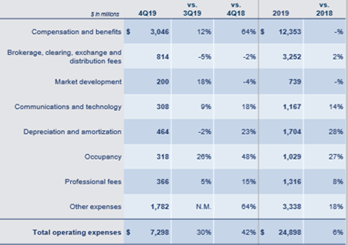

Total operating expenses for the quarter increased by 42% YoY to $7.3 billion on higher compensation, litigation expense, and expenses arising out of investments in growth initiatives. Notably, throughout 2019, GS reduced compensation expenses across many of its businesses to improve operating efficiency and to support incremental compensation expenses related to growth initiatives, where revenue production is beginning to materialize.

Source: Company Presentation

Net Revenues: Demonstrating strength in its relationship-based businesses and prominence in areas with relatively more recurring revenues, GS was able to beat street consensus estimates and increase its total net revenue for 4Q19 by 23% YoY to $9.96 billion.

Further, the company reorganized its business segment reporting in the quarter, which I think, facilitates a greater degree of comparability with peers and reflects GS’ ongoing commitment to transparency and accountability. The most notable change involves the elimination of the Investing & Lending segment and reallocation of its results to four new business segments which include Investment Banking, Global Markets, Asset Management, and Consumer & Wealth Management. The performance of each during 4Q19 is as follows:

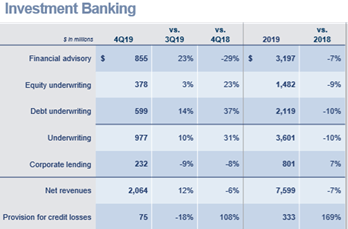

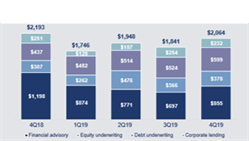

Investment Banking: Comprised of financial advisory, underwriting and corporate lending, the segment generated 4Q19 net revenues of $2.06 billion, down 6% YoY, primarily on lower industry-wide deal volumes, as reflected by financial advisory revenues of $855 million which were down 29% YoY. Nonetheless, the Investment Bank leads the M&A league tables, and management sees “continued strength” in its investment banking backlog, going forward.

Underwriting net revenues growth was strong, with strength seen in both equity and debt underwriting. Equity underwriting net revenues increased 23% YoY to $378 million, with particular strength in the US and European equity businesses, while debt underwriting net revenues were up 37% YoY to $599 million, reflecting higher asset-backed and leveraged finance equity. Corporate lending net revenues reached $232 million during the quarter on a net $28 billion funded portfolio of corporate loans in the investment banking unit.

Source: Company Presentation

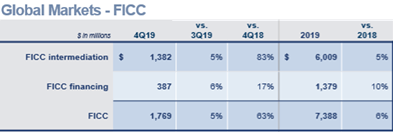

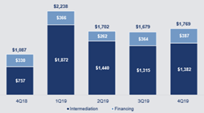

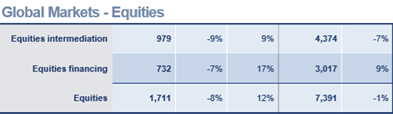

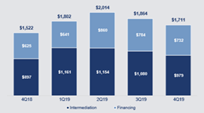

Global Markets: Comprised of fixed income, currency, and commodities (FICC) and equities, the segment witnessed a solid growth of 33% YoY to book net revenues of $3.48 billion for the quarter. FICC net revenues were $1.77 billion, up 63% YoY, driven by higher FICC intermediation revenues reflecting the continued strength of GS’ client-centric model and improved diversification of business mix.

Equities net revenues for 4Q19 were $1.71 billion, up 12% YoY, with a strong performance in both equities intermediation and equities financing. Equities intermediation net revenues rose 9% to $979 million in the quarter, as strength was seen in cash revenues in the US and Asia, and low-touch and block trading, which was partially offset by lower derivatives activity. Equities financing revenues were up 17% YoY to $732 million, reflecting improved spreads and higher client balances. Management highlighted that financing activity remains a strategic priority for the segment as it has historically exhibited attractive returns and considerable adjacent benefits to GS’ broader equities franchise.

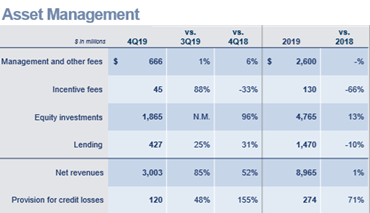

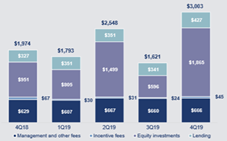

Asset Management: The segment, comprised of management, incentive, and other fees, equity investments, and lending, produced net revenues of $3 billion in 4Q19, up 52% YoY, driven by strong performance in equity investment, which generated $1.87 billion in net revenues. Management highlighted that ~90% of the gains in equity investments were event-driven, and the company saw material improvement vis-à-vis 3Q19 on certain large equity positions, including Avantor (NYSE:AVTR), Tradeweb (NASDAQ:TW), WeWork (WE) and Uber (NYSE:UBER) (gains of ~$400 million for FY19). A crucial point in this context is that GS plans to reduce the size of certain positions in the public portfolio ($2.4 billion in size at the end of 2019), which I think, is of lower quality, and has exited its position in Uber and reduced its position in Tradeweb.

Management and other fees related to client assets under supervision in the quarter increased 6% YoY to $666 million, while revenues from lending activities, which primarily relate to asset-backed loans, net interest income, and mark-to-market gains on debt investments, were $427 million, up 31% YoY.

Source: Company Presentation

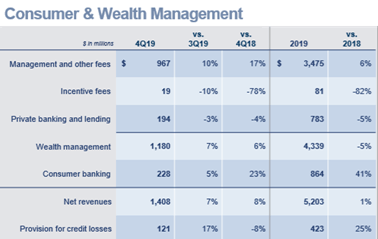

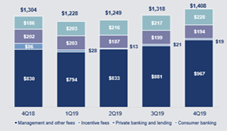

Consumer & Wealth Management: Comprised of wealth management and consumer banking operations, net revenues for the segment increased 8% YoY to $1.41 billion in 4Q19, driven by ultra-high net worth business, growth in Ayco and the newly acquired UnitedHealth high net worth business, and strong consumer banking growth.

Wealth management net revenues in 4Q19 increased 6% YoY to $1.18 billion. The growth was driven by management and other fees of $967 million (up 17% YoY), reflecting organic growth in the United Capital acquisition and was partially offset by lower incentive fees.

Consumer banking revenues increased 20% YoY to $228 million in 4Q19, reflecting higher net interest income. Total consumer deposits with GS at the end of the year increased 70% YoY to $60 billion across the US and UK. Funded consumer loan balances totaled ~$7 billion – $5 billion from Marcus consumer loans and $2 billion from credit card lending. Management pointed out that the slowing pace of the Marcus unsecured loan business growth reflects the anticipated growth in credit card lending from the launch of Apple Card.

Source: Company Presentation

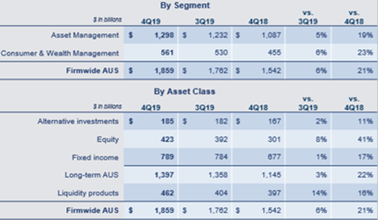

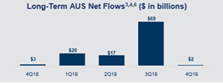

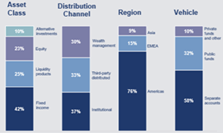

Assets under supervision: GS’ total assets from which it earns a management fee, including those in Asset Management and Consumer & Wealth Management, totaled $1.9 trillion in 4Q19 compared to $317 billion a year ago. The growth was driven by $108 billion of long-term fee-based net inflows from fixed income and equity (including United Capital acquisition), $65 billion of liquidity net inflows and $144 billion of market appreciation.

Source: Company Presentation

Strategy Updates and Outlook

Update on strategic initiatives: GS attracted an incremental $5 billion in consumer deposits during the fourth quarter of 2019, launched the firm’s first-ever credit card platform in partnership with Apple (NASDAQ:AAPL) during the year and completed the initial build of its digital transaction banking platform, processing over $2 trillion of payments on behalf of the firm. The rollout of the platform to third-party clients is planned for the first half of 2020 (some of the clients have already been putting operational deposits on GS’ balance sheet). In the meantime, the pre-tax loss associated with organic business projects, including Marcus, Apple Card, and transaction banking, totaled ~$700 million (~$1.85 per share) in FY19 resulting in a ~70 bps drag on ROE.

Future growth focus: GS is targeting a more recurring, corporate, bank-like, and technology-driven revenue stream from its investment banking and trading platform (~60% of total) and expects it to be augmented by a small share of other big revenue pools. This opens up a range of potential new market opportunities – the US consumer banking market (>$200 billion), cash management and transaction banking (>$115 billion), wealth management (>$100 billion), middle-market investment banking (~$20 billion), and private equity (>$15 billion). An incremental 1% share gain in each of these areas would result in $5 billion of additional revenues, driving an ~15% revenue growth over the medium term.

Nevertheless, investors have to be realistic and patient about these targets because it is going to take a number of years before some of these businesses can truly scale and contribute to ROE. The details and early progress is expected to be shared at the investor day later this month, but putting it all together, I think the new businesses, along with lower financing costs, better capital management, and operating efficiencies can add ~150-200 bps to the ROE in the next few years and ~300-400bps in the longer term as these businesses scale up.

Risk/Reward Skewed to the Upside

Despite a weak quarter this time around, I believe Goldman is headed in the right direction on its revenue growth initiatives. As its medium-term plan comes into focus, I think the market will eventually be willing to look past near-term uncertainties toward the medium-term achievability of a 15%+ ROTE target. Based on historical data, an ~15% ROTE would likely justify a P/B multiple well north of ~1.6x, driving material upside. With GS set for continued growth on promising top-line initiatives, TBVPS growth, and steady capital return via dividends and buybacks, I am decidedly bullish on GS heading into investor day.

Risks to the bull case include 1) the macro outlook, which could impact deal flow, equity/debt markets performance, and assets under management, and 2) litigation outcomes, particularly around 1MDB. That said, I think much of these risks are well-known and already priced into the current <10x earnings multiple, leaving ample room to surprise to the upside come investor day.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}