The record for the absolute worst dry bulk shipping spot rate of all time was set in February 2016, when the Baltic Dry Index (BDI) slumped to 219 points and vessel spot rates were just $2,000 per day. Four years later, that ignominious record may about to be broken.

The BDI is now in freefall, closing at 466 on Monday, down over 80% since September 2019. Rates for Capesize bulkers (vessels with capacity of around 180,000 deadweight tons) are now at around $3,500-4,000 per day — less than a third of breakeven rates in the low teens.

The two most important routes for Capesizes are the Brazil-China and Australia-China iron-ore runs. These two lanes now face pressures on multiple fronts, implying that rates have further to fall.

First, there’s seasonal demand weakness. Second, Brazilian iron-ore export regions are suffering debilitating floods. Third, there are too many ships in Australia.

Fourth, the IMO 2020 rule requires the use of more expensive low-sulfur fuel, slashing ship owner returns. And fifth — and most importantly — China is at severe economic risk from the coronavirus, which has the potential to dramatically curb dry bulk import volumes and spot freight rates.

How rates play out for Capesizes and smaller bulker classes has major consequences for larger U.S.-listed owners including Star Bulk (NASDAQ: SBLK), Golden Ocean (NASDAQ: GOGL), Safe Bulkers (NYSE: SB), Scorpio Bulkers (NYSE: STNG), Genco Shipping & Trading (NYSE: GNK) and Eagle Bulk (NASDAQ: EGLE).

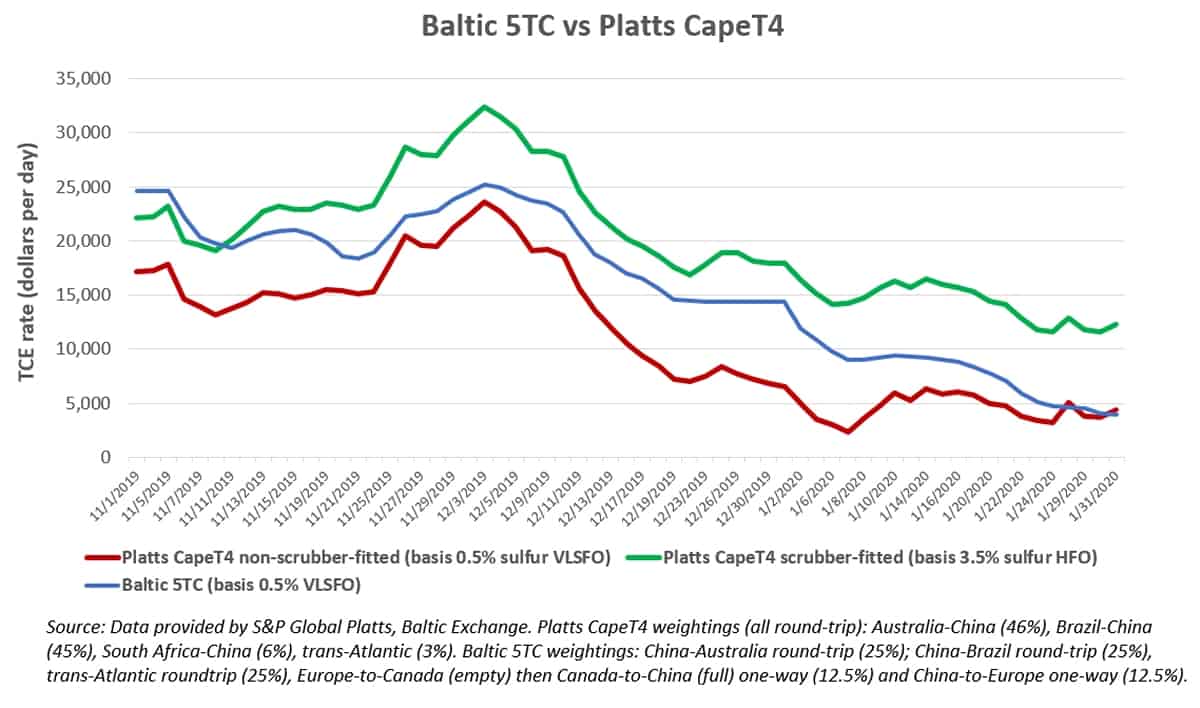

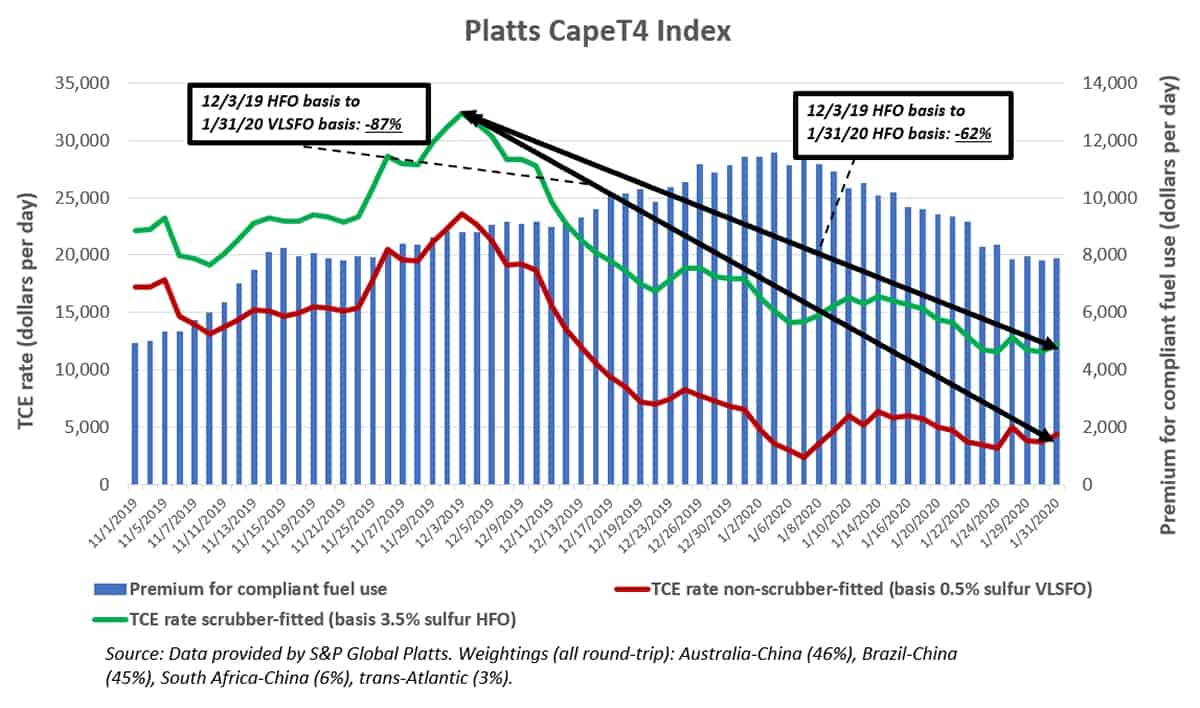

Global Capesize indices

The Baltic Exchange, and more recently, S&P Global Platts, compile global Capesize indices. The Baltic Exchange’s 5TC index was showing a time-charter equivalent (TCE) rate of just $3,973 per day as of Friday, Jan. 31.

A spot voyage is booked in dollars per ton of cargo. To obtain the TCE, the rate is converted to dollars per day and the cost of fuel is subtracted, meaning that the higher the fuel cost, the lower the TCE.

Due to the IMO 2020 rule, ships without exhaust-gas scrubbers are required to burn more expensive 0.5% sulfur fuel known as very low sulfur fuel oil (VLSFO) or 0.1% sulfur marine gas oil (MGO). Ships with scrubbers can continue to burn cheaper 3.5% sulfur heavy fuel oil (HFO). The Baltic Exchange 5TC is calculated on the basis of ships without scrubbers burning VLSFO.

The Platts CapeT4 Index has two parallel measures: one for nonscrubber ships burning VLSFO and one for scrubber ships burning HFO. (Only about 20% of Capes currently on the water possess scrubbers.)

Over the last week of January, the Platts nonscrubber CapeT4 index became very closely aligned with the Baltic 5TC; earlier in the month, the nonscrubber CapeT4 was lower than the 5TC.

The nonscrubber CapeT4 was showing a TCE rate of $4,349 per day on Friday. The CapeT4 scrubber index (calculated based on the price of burning HFO) was at $12,257 per day — in the vicinity of breakeven. In other words, scrubber-equipped Capesizes were earning $7,908 more per day due to the lower cost of HFO versus VLSFO.

Looking at the Platts scrubber and nonscrubber indices together shows the extent that dry bulk weakness is driven by seasonality and market factors on one hand, and IMO 2020 on the other.

What the curves reveal is that the underlying rate is continuing to fall due to worsening market conditions, but rates for nonscrubber ships have stabilized at around $4,000 a day because the spread between VLSFO and HFO is narrowing. In other words, the drop in VLSFO prices is preventing nonscrubber TCE rates from falling even further.

Platts calculated that the scrubber advantage peaked globally for Capes on Jan. 7, at $11,831 per day. If the VLSFO-HFO spread had stayed at that same elevated level, earnings for nonscrubber Capes would be at or near zero.

The most recent high for Capesize rates — $32,368 per day — was on Dec. 3, according to the Platts CapeT4. At that point, all ships were still burning HFO (the IMO 2020 rule went into effect Jan. 1). Between Dec. 3 and Jan. 31, scrubber ships saw rates fall 62%, whereas rates for nonscrubber Capes fell 87% (because of added fuel costs on top of seasonal declines).

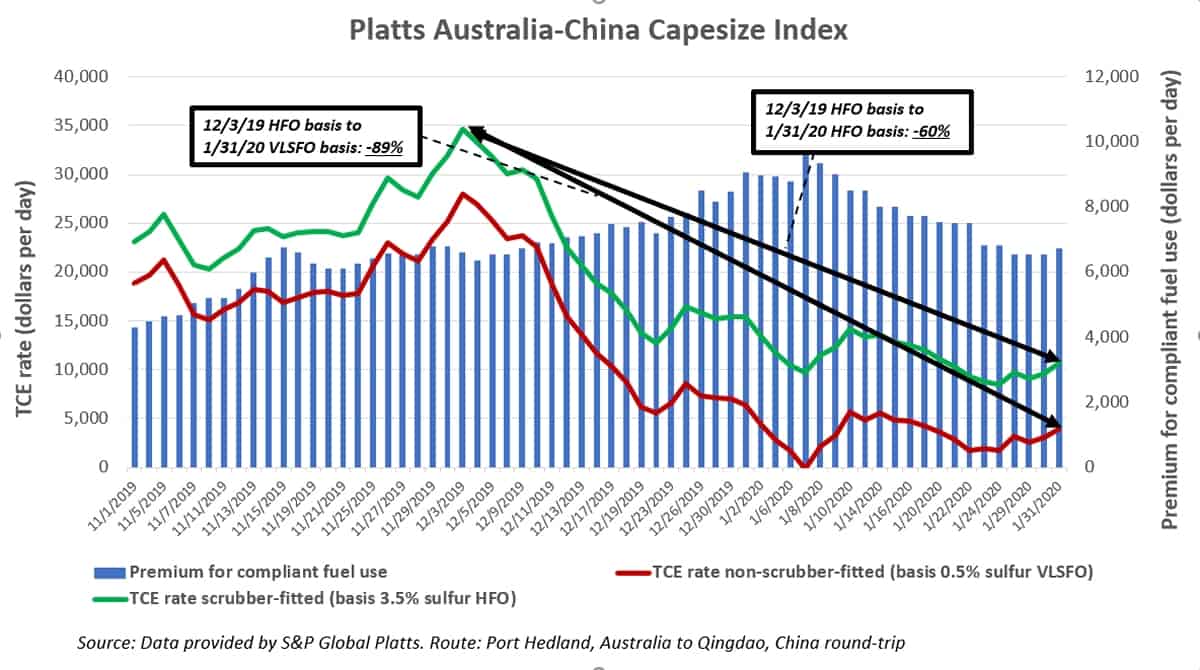

Australia-China route

Capesize performance has varied significantly between the various trade lanes.

By far the worst performer has been the Australia-China iron-ore market. Rates have fallen sharply despite the fact that volumes are up, meaning too many Capes are positioned in the Pacific Basin. Clarksons said Australian ore exports totaled 69 million tons in January, up 3% year-on-year.

Randy Giveans, the shipping analyst at investment bank Jefferies, told FreightWaves that as a result of the “flood” of Capesizes repositioning to Asia for scrubber installations at regional shipyards, there are too many vessels available for trading in the Pacific Basin, pushing rates to “artificially low” levels.

According to Yiannis Vamvakars, research analyst at Greece’s Allied Shipbroking, “The open tonnage list [ships available for hire] in the Pacific has already built up to unsustainable levels, a condition that is hard to shift if China doesn’t manage to take the [coronavirus] situation under complete control.”

For Capes without scrubbers, Platts assessed TCE rates at $3,900 per day on Friday. This marks an 89% decline from the latest rate peak on Dec. 3, taking into account the cost of the fuel transition.

Australia rates for scrubber-equipped ships have fallen 60% since Dec. 3, to $10,642 per day. The VLSFO-HFO spread has narrowed more in this market than in most others, bringing the scrubber earnings advantage for Capes down to $6,742 per day.

Meanwhile, unlike in most other Cape markets where underlying rates are slowly but steadily declining, the rate direction in the Australia-China market is less clear. Rates increased in the second and fourth weeks of January, bouncing off of extremely low levels.

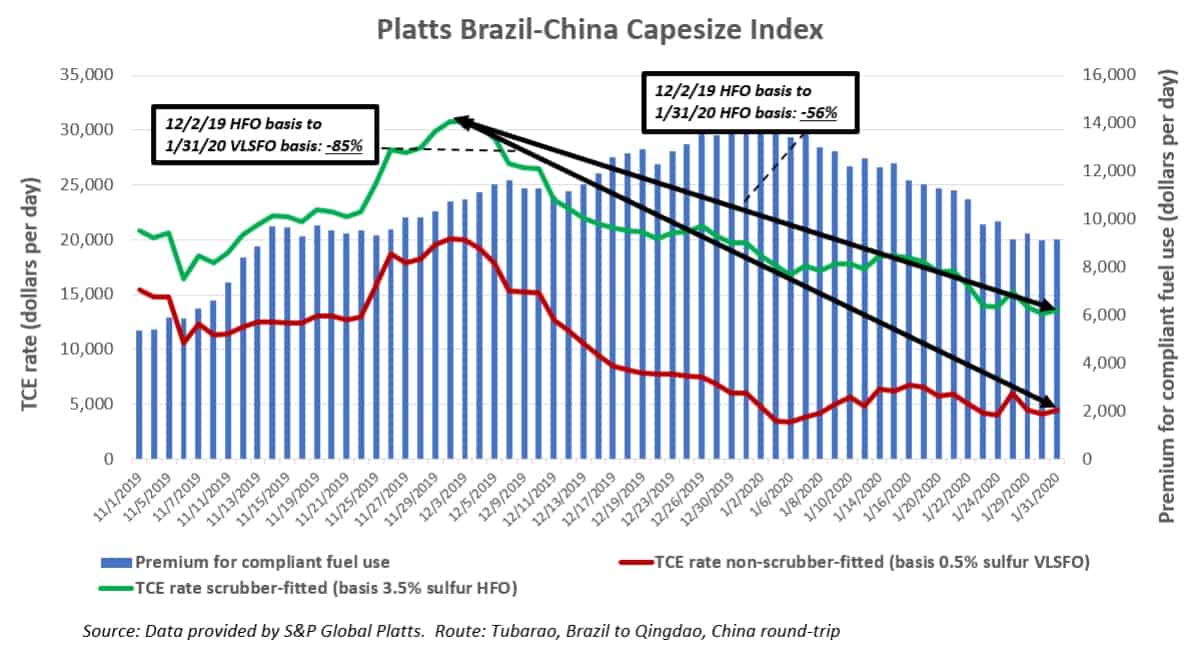

Brazil-China route

Brazilian iron-ore exports to China are particularly important to Capesize rates because the route is three times longer than the one between Australia and China, meaning it has three times the effect on vessel demand measured in ton-miles (volume multiplied by distance).

Brazil is suffering from heavy rains that have impaired the iron-ore production and export system of miner Vale (NYSE: VALE). Clarksons said that Brazil shipped out only 21.5 million tons of ore in January versus 32.2 million tons in January 2019 — a steep year-on-year decline of 33%.

Rates for Capes with scrubbers in the Brazilian export market have fallen 56% from their latest peak on Dec. 2, to $13,629 per day at the end of January, according to Platts. TCE rates for nonscrubber ships have fallen 85% over the same period, to $4,486 per day.

As in other markets, the VLSFO-HFO spread has narrowed, although it remains much wider than in the Pacific. Platts estimates put the scrubber TCE advantage in Brazil at $9,143 per day.

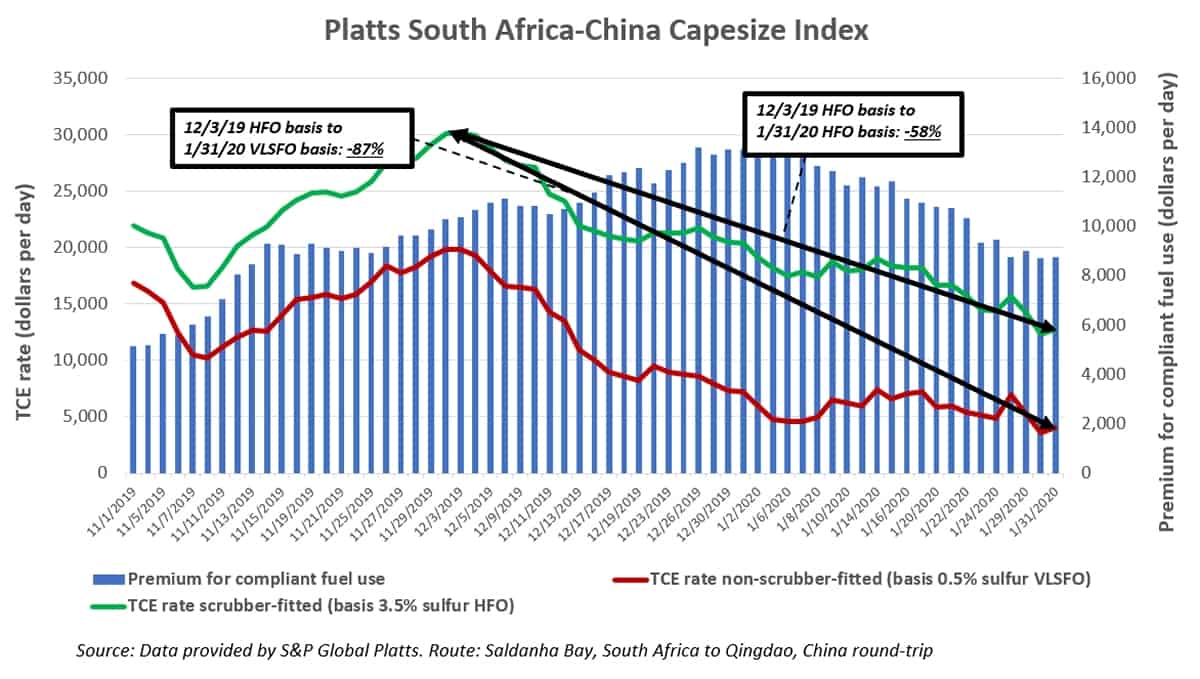

South Africa-China route

The third most important Capesize route is from South Africa to China. Rates here are moderately lower than in Brazil but higher than in Australia.

Platts assessed rates for scrubber ships at $12,745 per day on Friday, down 58% from the latest high on Dec. 3. Rates for nonscrubber ships have fallen 87% over the same period, to $3,994 per day.

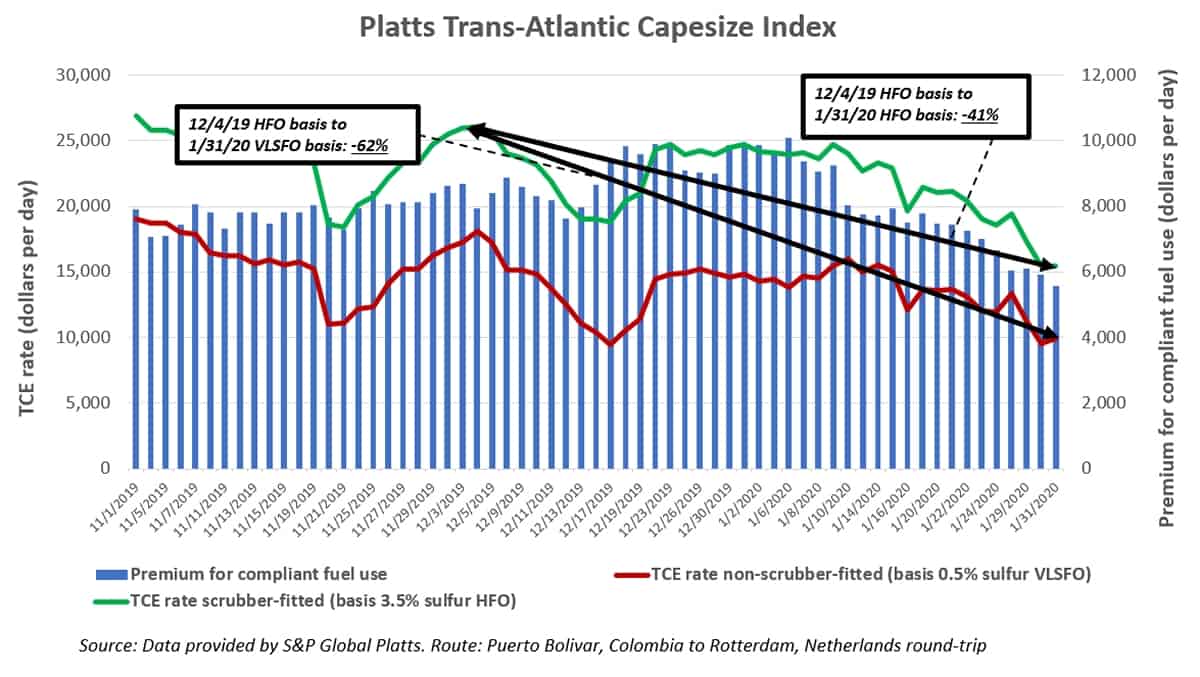

Trans-Atlantic route

Not all of the world’s Capesize routes are following the same rate pattern. One outlier is the trans-Atlantic market between Colombia and Rotterdam. (This route has only very minimal impact on the Platts CapeT4 Index.)

Scrubber ship rates have fallen only 41% since the most recent high on Dec. 4, and rates for nonscrubber ships have fallen only 62%. Scrubber ships were earning an estimated TCE of $15,545 per day on Friday and nonscrubber ships $9,884, with the fuel spread between the two unusually low at $5,570 per day.

Nonscrubber Capes are earning 2.5 times more loading in Colombia than they are loading in Australia, underscoring just how important vessel positioning can be to dry bulk earnings.

Future outlook

Seasonal headwinds will pass, but the coronavirus has thrown a major wild card into the mix.

According to Frode Mørkedal, managing director of research at Clarksons Platou Securities, “Weather problems will likely be temporary. The big question is, of course, what demand will be from China.”

On a positive note, Mørkedal pointed out that the freight derivatives market “is implying that second-quarter rates should average $11,000 per day and third- and fourth-quarter [rates] should average $17,000 per day. Thus, recent spot market weakness, which had generally been expected due to seasonality, should gradually give way to a healthier market as the year progresses.”

Giveans at Jefferies is also hopeful. “One-year time charter rates remain above $15,000 per day, leading us to expect a rebound later this year,” he affirmed. More FreightWaves/American Shipper articles by Greg Miller

{kind=link}