By April Joyner

NEW YORK, Feb 18 (Reuters) – A $4.5 billion buyout of Legg Mason Inc LM.N by rival Franklin Resources Inc BEN.N announced on Tuesday is the latest example of how a decade-long shift into low-cost, index-tracking products is pushing stock-picking funds to join forces to remain competitive.

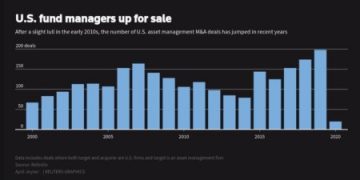

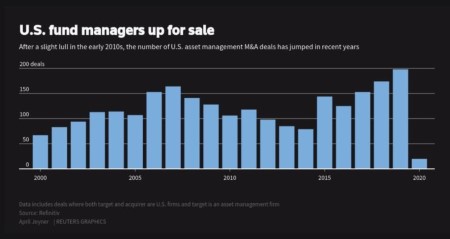

Mergers and acquisitions within the U.S. asset management industry have increased since 2014, according to data from Refinitiv. Nearly 200 deals took place last year, the most since at least 2000.

Past deals between stock pickers include Federated Investors’ 2018 purchase of a majority stake in Hermes Fund Managers, leading to the combined firm Federated Hermes Inc FHI.N, and Henderson Global Investors’ 2017 acquisition of Janus Capital to form Janus Henderson Group PLC JHG.N.

The comparatively low costs of exchange-traded funds have forced actively managed funds to slash their fees, pushing active firms to merge in order to preserve their profits, said Larry Tabb, founder of capital markets research firm Tabb Group.

“It forces what used to be storied asset management firms to start acquiring or be acquired,” he said. “The larger funds need to become even bigger.”

The largest passive managers now eclipse active funds in assets under management, which has helped to spur consolidation.

In 2019, passive U.S. equity funds overtook active funds in net assets under management, according to Morningstar Direct. As of Dec. 31, passive U.S. equity funds managed $4.78 trillion in net assets while active funds managed $4.58 trillion.

BlackRock Inc BLK.N alone has more than $7 trillion in total assets under management, while Vanguard Group has more than $5 trillion. A combined Franklin Resources and Legg Mason would manage about $1.5 trillion in assets.

At the same time, since the bull market for U.S. equities started in 2009, passive large-cap funds have largely outperformed their active counterparts, according to Morningstar Direct.

Last year’s performance followed that trend. Passive U.S. large-cap blend equity funds – in which neither growth nor value stocks dominate – posted a 30.1% return in 2019, whereas active U.S. large-cap blend equity funds returned 27.8%. The benchmark S&P 500 .SPX index rose 28.9% last year.

U.S. fund managers up for sale pnghttps://tmsnrt.rs/37HaEm2

The rise of passive funds pnghttps://tmsnrt.rs/39LjrF3

Active managers eclipsed by passive giants pnghttps://tmsnrt.rs/38A6cH7

Active management, smaller returns pnghttps://tmsnrt.rs/2P8qhN8

(Reporting by April Joyner; Additional reporting by David French in New York and Ross Kerber in Boston; Editing by Ira Iosebashvili and Dan Grebler)

(([email protected]; +1 646 223 7480; Reuters Messaging: [email protected]; Twitter: @aprjoy))

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}