Trend Investing recently interviewed three key EV metal supply chain experts to get their views on:

- Electric Vehicle (EV)/Internal Combustion Engine (ICE) vehicle purchase price parity timeline.

- EV market share in 2025.

- Where in the EV supply chain they see the best investment opportunities going forward.

- Their ranking of investment opportunity across the EV metals (lithium, cobalt, graphite, nickel, manganese, copper, and NdPr).

- Where they see the next EV related boom area.

Our three EV metals and supply chain experts’ brief background

Andrew Miller (Benchmark Mineral Intelligence) Product Director @BenchmarkMin | Supply Chain Analysis | Lithium-ion Batteries | Price Assessments | Lithium, Graphite, Cobalt, Anodes and Cathodes.

Chris Berry – House Mountain Partners – @cberry1 – Based in New York, Chris has been an independent analyst since 2009 with a focus on Energy Metals supply chains, including lithium, cobalt, graphite, vanadium and rare earths.

Adam Panayi (Rho Motion) – Managing Director @rhomotion – Rho Motion provides long-term forecasts and analysis of Electric Vehicle battery pack size, chemistry and costs.

Experts Interview

1. In what year do you expect electric cars to become the same price as conventional (ICE) cars on a purchase price basis only?

Andrew Miller

Our research at Benchmark Minerals is focused further upstream, but downstream experts such as Rho Motion would indicate price parity being reached by around 2024. This will vary depending on the type of lithium ion chemistry being deployed, and therefore, this timing will vary across different applications.

Chris Berry

I think the date is dependent upon what type of transportation you’re referring to. I could see fleet-level electrification for last-mile delivery happening sooner than many believe (perhaps 2023), as larger companies such as Amazon (AMZN) or FedEx (FDX) have the scale and balance sheet to shoulder the costs associated with switching over to fully electrified transportation. Additionally, many of these companies are intent on burnishing their “green” credentials and adhering to strict ESG mandates, so may be willing to go fully electric even if the unit economics don’t make sense at first.

Regarding light duty vehicles, again, there is a great deal of guess work here, and I think the economic tipping point for a full EV to beat an ICE on cost will vary based on geography, with China likely leading the way here as early as 2023. This has more to do with driving habits and battery chemistry choices than anything else.

If battery factory capacity is built out as planned, then the rest of the world may follow suit by 2023-2024, though we have seen how enormously sensitive the market is to EV subsidies. The tightening or removal of subsidies is positive overall, as it forces companies to innovate, but consumers have demonstrated that there is a great deal of price elasticity here.

Adam Panayi

Based on our analysis of emissions legislation, battery cell development and OEM plans for EV roll-out, we have developed a BEV cost and price model which incorporates battery cell, module and pack costs, as well as BEV platform costs and OEM margins. An important, and somewhat overlooked, issue is the development and scaling of pure BEV platforms, which offer the opportunity for significant cost savings over time. Another crucial issue is the fact that OEMs are prepared to make no margin, and in reality losses, on their initial EV model line-ups while they build scale. Finally, we expect that ICE vehicles will become more expensive over time as emissions legislation tightens and places greater technological cost burden on OEMs. As such, we expect purchase price parity in 2024 or 2025.

2. Where do you see global EV market share by 2025? (E.g.: 10% etc.)?

Andrew Miller

In our models, we see penetration of between 10% and 15% by 2025.

Chris Berry

Again, dealing in any sort of prediction or forecasting is a mug’s game, but thinking in terms of probability and embracing the volatility is likely a better methodology. That said, I see a low probability that we hit a 10% EV penetration rate by 2025. The reason is that I don’t see the full lithium ion supply chain adjusting in time to handle the potential demand. Battery pricing will certainly be lower by 2025, and OEMs will be forced incentivized to electrify their fleets, but I’m not sure if this is enough to encourage a mass switch from ICE to EV. In addition to this, we are in the late cycle of an economic expansion. While there is no clear way to know when this ends, when it does, auto sales will almost certainly suffer. When the cycle begins anew, will EVs be cheaper than ICE cars and will consumers just automatically make the switch? This underlies the bullish EV thesis, but it remains to be seen.

Adam Panayi

EV penetration is a function of the interaction between government legislation, both on the emissions side but also on subsidies and incentives, and OEM strategies to meet these standards, as well as consumer acceptance of the technology. We look at every market and OEM in detail in order to obtain a balanced and robust perspective. As such, our headline figures for global EV sale penetration are 11% by 2025 and 28% by 2030.

3. Please comment on where in the EV supply chain you see the best investment opportunities going forward (EV manufacturers, battery manufacturers, cathode or anode manufacturers, miners).

Andrew Miller

There is a lot of value to be realised at the raw material end of the supply chain, especially for companies producing the advanced materials required by battery anode/cathode producers.

The key battery raw materials – lithium, cobalt, nickel and graphite – all face their own supply chain challenges to scale up at the rate required by auto/battery consumers, so producers that are able to supply into this sector will benefit from the need to secure material in the long term and potential volatility in pricing in the medium term.

Chris Berry

If you are looking at upstream opportunities, it is important to remember that the lowest-cost producer always wins, and I would prefer those plays with strong partnerships (technical know-how and balance sheet strength) and geologic and geographic diversity. Further downstream, I am mainly focused on looking at technologies that can increase production efficiencies, minimize reliance on raw material volatility, and capture margin along the supply chain (vertically integrate), such as cathode production or lithium ion battery recycling. Nano One (OTCPK:NNOMF, NNO:TSXV) is a good example, or recyclers with a focus on hydrometallurgical processing are also alluring. In the interest of full disclosure, I am an advisor to a privately held lithium ion battery recycling company, and can vouch for the increasingly compelling economics.

Adam Panayi

A big area that is overlooked is on the charging side – it’s only just starting and there’s a real opportunity to lead in the space. At present, there’s a large number of smaller operators active in the market. Given the level of capital investment that will be needed in charging infrastructure over the coming decade, there will have to be some consolidation in the area in order for companies to operate at a scale that will make them viable.

4. Can you please rank the EV metals (lithium, cobalt, graphite, nickel, manganese, copper, and NdPr in your preferred order and comment on your top pick(s) and why you like that sector for the next few years?

Andrew Miller

Lithium, nickel, cobalt and graphite are the most critical inputs over the coming few years because of the restricted supply structure in each market and their use across the predominant technologies that will be used in passenger EVs.

Lithium as the mainstay material across portable battery technologies mean it remains central. Nickel will benefit from the shift towards higher-energy density cathode materials, and graphite is the mainstay anode material in existing lithium ion technologies that will dominate for at least the next decade. Cobalt, while being used in lower intensities, will still benefit from the scale of battery demand and faces the added challenge of being the smallest market by volume and only being produced as a by-product.

Chris Berry

Lithium, nickel, copper, NdPr, cobalt, manganese, graphite. The lithium demand story speaks for itself, and I won’t belabor the obvious here. Battery-grade lithium supply will lag demand, and a long-term incentive price of $11,000/t is highly probable.

I’m not convinced that demand from electrification alone will move nickel and copper structurally higher. The markets are just too big to feel a pinch from EV-related demand. You need to see strong economic growth (lower probability) coupled with geopolitical tensions (higher probability) to really move these markets.

While I like the NdPr story, China still looms large here, and I think it’s a seven-year wait to achieve any sort of significant non-Chinese supply chain. I’m happy to be wrong here and am pleased to see Western governments getting involved, but don’t think any moves will be made overnight.

Adam Panayi

Graphite – If you have a resource with the right grades, then the potential growth is huge, the market is currently oversupplied and undervalued, but the prospects are good, and despite silicon and sold state anodes on the horizon, the mass market for anodes will be graphite-based.

Cobalt – For a pure-play cobalt project in a good jurisdiction, of which there are only a handful, the prospects are great; cobalt is more difficult to get rid of than is commonly assumed.

NdPr – Vital from a motor point of view and relatively under-researched from an investment standpoint.

Lithium – High-profile from an investment point of view, with a lot of media exposure, still a good bet with the right project given where prices are now.

Nickel – Lithium ion NCM batteries are actually nickel batteries when looking at the overall balance of materials; the movement is towards higher nickel in batteries, whatever happens with everything else.

5. If possible, can you name some EV-related stocks or sectors where you see the best investment opportunities ahead for investors? Or perhaps any areas that may be the next EV-related boom area?

Andrew Miller

We don’t recommend particular companies, but we think the companies best-positioned to benefit from rising EV demand are those that have control of resources and the advanced materials needed by the battery supply chain. Those that are strategically located close to existing or future markets will also have the added benefit of providing supply security.

Chris Berry

I answered this one earlier, but on the upstream raw materials side, I like lowest-cost producers with geologic and geographic diversity and strong and stable partners. As mentioned above, cathode technologies and recycling are exciting areas of growth. I have also spent time in recent years on direct lithium extraction technologies (DLE), and while I like what I see, I think these technologies will be incremental or additive to existing producers rather than revolutionary.

Despite the bumps and bruises we’ve all sustained in recent months, it’s important to remember that the EV thesis is still well intact. Investors need to think hard about where we are in the capital cycle, as this drives risk appetite and volatility in the sector overall. As margins shrink as you go further down the lithium ion supply chain, a diversified portfolio of plays along the supply chain with a margin of safety embedded offers the highest probability of outsized gains in the future.

Adam Panayi

We don’t offer advice on individual stocks, but in a market where there is so much hype, and in some cases misinformation, the key point is to take an objective view on companies that are at limited risk of technological substitution, have the best opportunities for sustainable growth, and are currently undervalued owing to the stage of the investment cycle that we are currently in. At all points in the supply chain, from raw materials to charging, these opportunities exist.

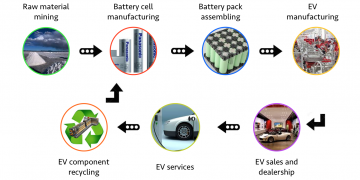

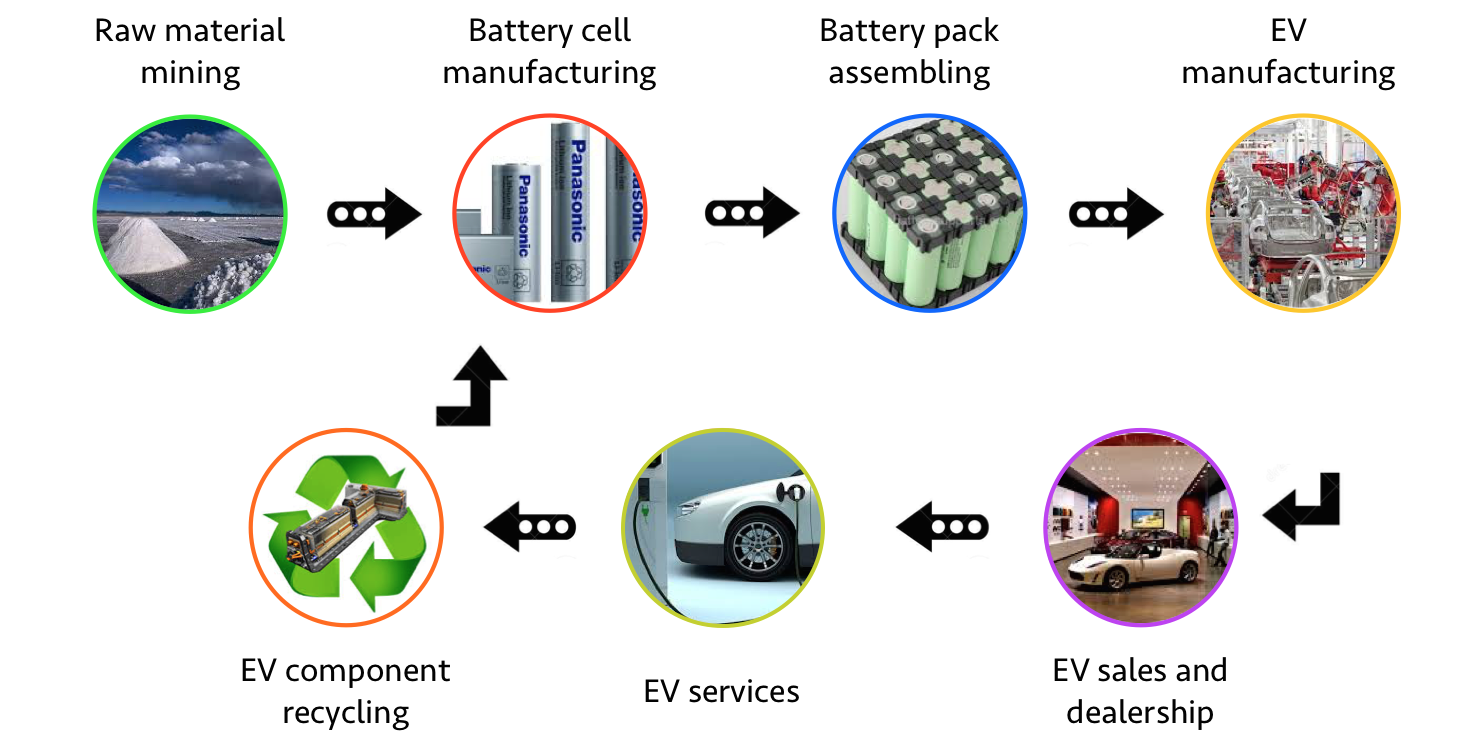

An EV supply chain diagram

(Source)

Conclusion

Some takeaways for investors from the 3 experts are that they mostly see EV/ICE parity by 2023-2025. By 2025, they see EV market share as 10-15%, <10% and 11%. For best EV supply chain opportunities, they see the miners (lithium, cobalt, graphite) that can supply battery quality feed, well-partnered companies and companies that can produce the technologies that can increase production efficiencies, and the EV charging sector. Our experts also liked low-cost producers, in safe locations and close to their supply chain.

I would sincerely like to thank our three experts, Andrew Miller, Chris Berry, and Adam Panayi, for giving freely of their time and their extensive wisdom and experience in the area of the EV supply chain and metals. As leaders in the industry, their insights are widely sought-after and well-valued.

As usual, all comments are welcome.

Trend Investing

Thanks for reading the article. If you want to sign up for Trend Investing for my best investing ideas, latest trends, exclusive CEO interviews, chat room access to me, and to other sophisticated investors. You can benefit from the work I’ve done, especially in the electric vehicle and EV metals sector. You can learn more by reading “The Trend Investing Difference“, “Subscriber Feedback On Trend Investing”, or sign up here.

Latest Trend Investing articles:

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The information in this article is general in nature and should not be relied upon as personal financial advice.

{kind=link}