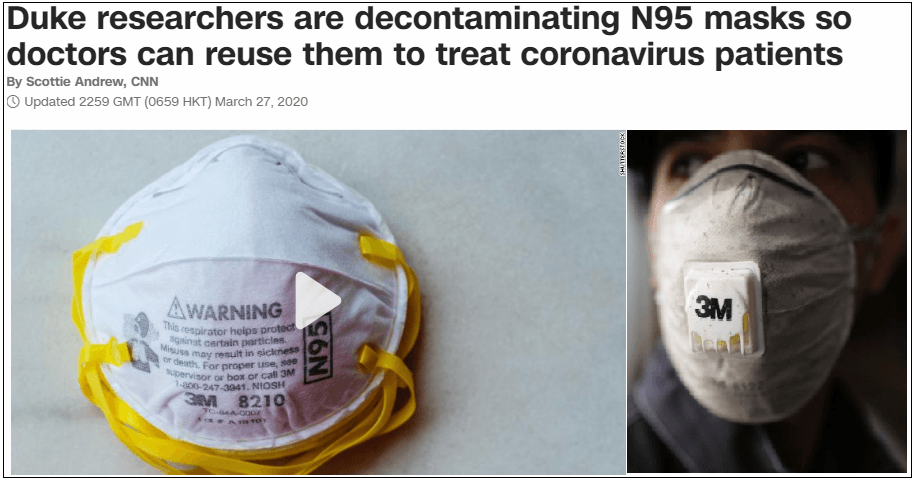

3M (MMM) is a technology company having customers in practically all countries of the world. It has been restructured and now operates through four segments compared to five previously.

The reason for my interest to invest in the company is because it manufactures the N95 respiratory mask which, in absence of a vaccine, is so important in the fight against the coronavirus.

I look at the company’s revenues, gross profit margins and supply chain. I also evaluate its capacity to meet the current demand for respirators as well as consider the risks in an environment characterized by increased suffering and a higher degree of uncertainty.

Stagnant revenues but higher gross profits

While there has been some revenue growth in the last quarter, the cost of revenues has been decreasing and this, over the last three quarters. This has in turn resulted in higher gross profit margins (% Gross profit).

Gross profit margin = (Revenues – Cost of Revenues)/Revenues * 100

Figure 1: Income statement in the last three quarters in millions of USD

Source: Seeking Alpha

Falling costs of raw materials (petroleum based materials, minerals, metals and wood pulp) as well as better supply chain management and inventory management have contributed to a decrease in cost of revenues.

The company has seen success in managing its supply chain. For example, in the US, despite coronavirus induced interruptions, the company has avoided major supply chain disruptions by sourcing materials for its protective face masks from regional suppliers.

The company has used technology in the form of Enterprise Resource Planning (ERP) system to improve the supply chain and get a better idea of its inventory as from 2017, well before the downturn. A high inventory level means more goods, either raw materials or finished goods lying idle. The inventory level for 3M, which was reduced by USD 370 million in the year 2019, is targeted to be further cut by USD 500 million in the years 2020 and 2021, meaning more cash generated from operations.

However, despite rising gross profits, the company has suffered from a lower operating margin. The reason for this is additional SG&A, R&D and not forgetting those restructuring costs pertaining to staff voluntary retirement as management had already foreseen a downturn in sales for the year 2019 and Q1-2020. As a result of this higher non-recurrent cost incurred in the year 2019 accounts, there should be lower administrative cost (OPEX) down the line.

I next analyze the reasons for the stagnant revenues with the aim of identifying the opportunities for the year 2020.

Significant potential revenue gains

3M’s revenues from the Asia-Pacific region account for roughly a third of its total revenues. Now, with demand for its products starting to fall as from the latter half of 2017 and continuing right through the second quarter of 2018 because of weak customer demand in China, the revenues have been falling as well.

The subsequent U.S.-China trade war made matters worse for 3M.

Figure 2: 3M Company and Subsidiaries Consolidated Statement of Income Years ended December 31

Source: 3M Annual Report

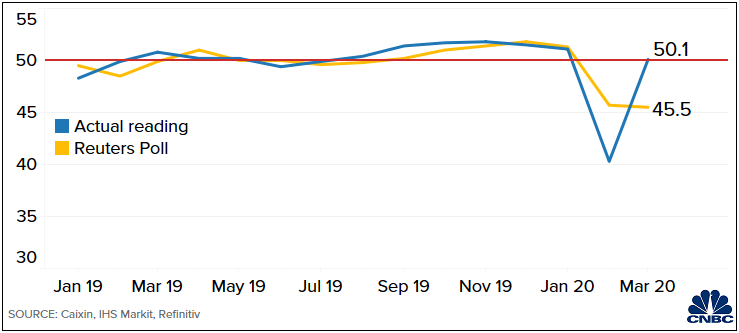

Now, with business confidence improving in China, as evidenced by the survey on China manufacturing PMI, it can be reasonably expected that 3M’s industrial and electronics business segments which serve a range of markets, such as automotive equipment manufacturers and construction sectors will benefit.

Figure 3: China Manufacturing PMI

Source: Caixin IHS Markit, Refinitiv published in CNBC

However, this improvement in business confidence should be monitored closely by investors as there are still demand challenges ahead. Any sustained growth in the Chinese manufacturing sector would start to impact earnings only as from Q2-2020.

On a more positive note, the company’s respirator manufacturing plants in China have already been busy working to provide much needed respiratory masks to hospitals and the public.

I estimate that just for the respiratory equipment business, considering the wider global market, there should be revenues of about USD 1.2 billion factoring in 1.5 billion masks based on a unit price of 80 cents. These masks are being primarily sold to governments and hospitals empowered by large stimulus packages.

Also, given their scarcity, these masks are now being referred to as the new “white gold”.

Now, I look at two other sources of revenues for 3M in the context of the fight against COVID-19.

Additional potential for revenue growth

First, 3M has entered into a partnership agreement with Ford (F) to boost production of the PAPR (Powered & supplied air respiratory protection) equipment which it already manufactures. The aim is to increase production to more than 5 times current capacity.

Figure 4: Powered & supplied air respiratory protection

Source: 3M Safety products

With a PAPR costing USD 2000 and the company having to produce just 100,000 units (a quick guess given the deteriorating health environment), I estimate the revenues to be around USD 200 million.

Second, there are the air purifier filters. These can efficiently capture particles that are the size of the COVID-19 virus, and can therefore help protect against infection. However, scientists are still researching how the virus spreads, and the current consensus is that it is not an airborne virus.

However, I believe that this uncertainty as to the mode of spreading will not deter offices from buying the Virus HEPA Room Air Purifier Filter being sold by 3M for HVAC (building air conditioner) systems.

The USD 383 million which the company is deriving from the consumer healthcare segment could shoot up in the longer term as the HEPA filters which are currently used in critical care environments within healthcare facilities find a wider utilization both at home and in the office.

3M has also seen demand soaring for other items like sanitizers and disinfectants.

With surging demand for the company’s product and potential revenues of USD 1.4 billion excluding the HEPA filters and sanitizers, I next turn my attention to the supply side of the equation.

Making use of Surge capacity to satisfy demand

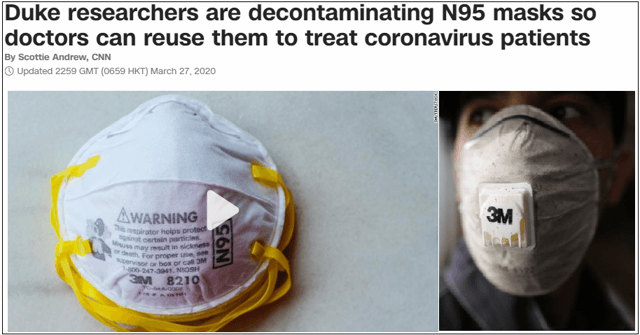

3M is under pressure by the government and hospitals in the US and around the world to produce more masks. These masks worn by physicians, nurses and other hospital staff as well as more and more by people when going out of their houses, are in short supply. In some cases, they are even being re-used.

Figure 5: 3M Respirators

Source: CNN and Yahoo Finance

According to Mike Roman – CEO speaking during JP Morgan Industrial Conference on March 10, 2020:

We’ve seen some impact on softer demand in areas like China and then we’ve seen of course, the ramp up and demand on respiratory protection. So we’re actually executing on both sides of this today. We’re going to watch it closely. We aren’t — right now, we don’t — with that — what I just described to you, we aren’t executing anything else, but we’re watching closely.”

The company is using two strategies to produce respirators:

- Surge capacity

- Local sourcing as part of improved supply chain

Additional capacity is being utilized at the Aberdeen plant using contingent machinery which had been installed to respond to demand from the teams fighting wildfires in Australia. Moreover, the company had also built surge capacity in its respiratory factories throughout the world to address demand bursts following lessons learnt during the SARS epidemic. On the other hand, Honeywell (HON), another manufacturer of respirators has to hire 500 people to expand capacity.

This said, despite boosting supply, the company is aware that there will still be a shortage in the supply of respirators, at least in the short to medium term. This shortcoming in supply has to be filled through imports as well as by other manufacturers including Honeywell, one of 3M’s competitors.

Competitors

The gross profit margin for 3M which stands at a figure of 48% is the highest.

Figure 6: Comparing with competitors, Honeywell and General Electric (GE)

Source: Seeking Alpha

I already discussed about the Gross profit margin earlier as a measure of the cost of revenues and again invoke this important metric, this time as an indicator of management efficiency in using labor and supplies in the production process. In an uncertain environment where the company cannot accurately forecast sales, drops in demand can be compensated to a large extent by being efficient on the production side.

Also, 3M dividend yield at more than 4% is mouthwatering and the company generates more than USD 7 billion cash from operations.

However, this analysis will be biased without identification of the risks.

Risks (Debt, oil price rising, employee infection)

First, I also look at debt. As can be seen from figure 6 above, 3M has USD 18.5 billion of debt. However, it also has US$7 billion in cash, and so its net debt is USD 11.5 billion. Now, as at December 31 2019, it had USD 9.2 billion of current (short term) liabilities. Also, the company has a total five-year revolving credit facility of USD 4 billion expiring in November 2024. Therefore, even at a high figure, the debt is still manageable.

With respect to liquidity, the company has a staggered maturity profile, for ease of refinancing with an amount of USD 1.8 billion maturing in the present year (2020).

Also, the cash position which has already been increased through decrease in inventory and accounts receivable looks to be augmented further as the company’s efficient supply chain contributes to lower inventory through better interaction with suppliers. Also, with the Federal Emergency Management Agency (FEMA) distributing N95 masks to healthcare organizations in states hardest hit by the pandemic, there looks to be no distribution disruption.

3M had an A1 credit rating with a stable outlook from Moody’s Investors Service. However, this outlook has recently been downgraded to negative from stable. This is an important item to consider for investors, but as a front liner stock in the defense against COVID-19 and with USD 180 billion earmarked for the healthcare sector under the CARES act, 3M has a guaranteed market and its customers have the capacity to pay.

Second, I consider the risks with respect to raw materials like metals and oil on which the company’s manufacturing units depend on. With oil price such low, many producers may opt to shut down oil rigs and there can also be supply disruptions all resulting in a sudden rise in the price of oil.

Same is the case of metals where decrease in production (mining activities) may lead to price increases. Here, the mitigation factor is that the company manages commodity price risks through negotiated supply contracts and price protection agreements and commodity price swaps. These hedging measures can help to protect against the costs of raw materials to some extent.

Third, I next consider the production risk in case any of 3M’s employees are infected with factory output suffering from disruption as a result. In this case, it is important to note that the company has already put in place strict social distancing measures including yellow tapes boundary identifiers which restrict the movements of staff.

Other risks (litigation, alignment with the aims of the federal government)

Fourth, there are litigation charges which can impact the cash flow. In this respect, the company is a defendant in two litigation cases, the first with relation to PFAS (certain per-flourinated compounds) environmental-related matters and the second relating to a coal mine dust respirator mask lawsuit. This caused operating income margins to decrease 2.8% in 2019 when compared to 2018.

However, in this case, while such litigation cases can take years to be settled, it is noticed that such charges have been decreasing year-on-year and that the company has been able to time associated payments in such a way so as to mitigate impact on cash position.

Finally, there also has been some “hot discussions” between the US authorities and 3M’s management concerning distribution and exports of masks and some investors may fear that in case of escalation, the company may be nationalized.

However, this would clash with the laissez-faire government policies and the only time when government took stakes in private enterprise was during the last century with coal mines and railways. Moreover, at the peak of the economic crisis in 2008, there was considerable talk about government taking ownership stakes in US banks but it did not happen.

I have tried to cover the maximum number of risks but none of these look strong enough to constitute a headwind for 3M.

Valuations

First, I take into consideration that 3M’s stock price has declined by 30% since the beginning of 2018. It fell from USD 250 in January 2018 to about USD 180 in June 2019. Over the same period, the S&P 500 rose by 4.2%.

Second, I take into consideration that oil is a very important raw material and that for every USD 10 rise in the price of oil, the impact for 3M in terms of earnings is a fall of $0.02 to $0.03 and vice versa. Also, the EPS of USD 9.30 to 9.75 provided in the Year 2020 Guidelines was based on oil at a price of USD 50 whereas the price is in the USD 25-30 range currently. Using an estimate of 30, we have an EPS of USD 9.35 to 9.80, which is higher than the figures provided in the guidelines.

Third, the 3M’s range of product is recognized internationally, is a trusted brand and customers are prepared to pay the price. Also, this is no ordinary epidemic and medical authorities simply want the best. According to estimates, potential revenues of USD 1.4 billion and above are possible just for medical devices.

Hence, the stock price should be at a minimum of USD 160. It is to be noted that I am not overly optimistic as there are real demand concerns for the company’s products in the industrial and electronics business segments and there are risks.

I am looking to buy at USD 130-135 price level.

Key takeaways

3M, through technology and restructuring has undergone significant transformation especially in terms of the supply chain.

Also, in a business environment with low sales figures, being able to reduce the inventory level is critical. This is translated into above-average gross profit margins.

Moreover, compared to competitors, who are scrambling to boost up production capacity to produce vital health devices, 3M already has some surge capacity inbuilt and is therefore responding more rapidly to increasing demand.

However, there are risks, especially with regards to that debt level and the wider economic environment but in view of the cash generated from operations and the strategic importance of the company’s products in the fight against COVID-19, the company should not face any hurdle to get re-financed.

For the longer term, expansion of the Health Information System division, which forms part of the healthcare business group, should generate considerable growth.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in MMM over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}