I was in Hamburg this week, where my contacts, rather surprisingly, barely mentioned DHL Global Forwarding, Freight (DHL GFF) and the latest performance of its air, ocean and road freight activities. Perhaps I landed in the wrong city, I silently complained mid-way through its interims on Tuesday.

Most of the talk surrounded DB Schenker and its next corporate structure travails and steps – most likely caused by Berlin rather than self-induced – alongside the prospects of both the major local carrier, Hapag-Lloyd, and top management decisions at AP Møller-Mærsk.

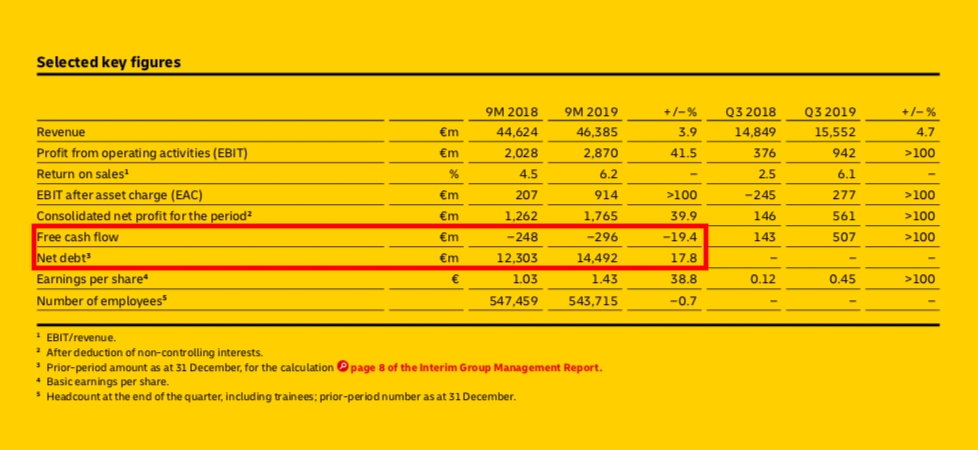

But just as Germany narrowly skirts recession, the resounding success DHL GFF has become after years of struggles surely deserves a mention. Its nine-month results (9M 19) were the brightest for its own comparable corporate data set firmament, setting a new record for the unit in terms of operating earnings (ebit) and operating cash flows (OCF) for this major asset-light business.

The usual caveat is that its numbers are barely acceptable compared to the high standards of its closest peer, Kuehne + Nagel (K+N), although they are a lot less disappointing when compared with its rampant public rival, DSV Panalpina (DSV PAN), which remains virtually indecipherable on a comparable basis, as it lately consolidated only about six weeks of trade and financial data for its newly acquired toy, Panalpina.

As it did in recent quarters – under the leadership of ex-K+N and now DHL GFF CEO Tim Scharwath – DHL GFF shone in the third quarter as part of a group that is holding up nicely, although any bear would be comfortable arguing that the stock market valuation of the Deutsche Post DHL Group (DP-DHL) is justifiable only if extraordinary corporate activity of some kind is on the cards – its mid-term guidance clearly errs on the bullish side of corporate projections, among other things.

Barring DHL GFF, its other three-and-a-half pillars (“e-commerce solutions” has just recently been created) are unlikely to be marked up by investors – there are not comparable public assets against each DP-DHL unit, anyway – so there are few options really on the road to monetisation of assets.

(Source DP-DHL)

Now look at the table below: 9M 19 ebit was a whopping €348m, a record for the period since the data became available in 2008 (DP-DHL split up internally its logistics unit, previously comprising supply chain and DHL GFF, effective 1 January 2008).

(Source DP-DHL)

Its operating cash flow line was even more stunning at €415m, both in absolute and relative terms.

Cash flow productivity speaks volumes about the level of efficiency that has been sought by Mr Scharwath since mid-2017 – it compares with €410m of (adjusted) OCF in 2012, which was the previous high. Consider that its normalised ebit over the past few years – excluding 9M 19 and 9M 12 highs – stands at about €134m.

(Source DP-DHL)

Now its OCF implied a 3x multiple against the average, which inherently means Mr Scharwath’s bidding to make the business more predictable against the volatility of ebit/OCF of the past – even more remarkably (see the tables above and below), this happens as it’s tough out there. These are not the “good days”.

(Source DP-DHL)

Bear in mind these comparisons are not perfect throughout the data series – several adjustments must be made, from inorganic considerations to accounting chicaneries and the like. However, a headline regression analysis since 2008 – I can share here a quantitative hand-written summary where the relevant data is highlighted – shows that DHL GFF has grown revenues to €11.2bn from €10.4bn, hence at compound annual growth rate (CAGR) of 0.6%, against 1.7% for its ebit.

Take the mid-point of the series before the 2015 annus horribilis (the IT meltdown under Roger Crook), and its earnings growth rate has been either in line or above revenues.

Most comparisons where the final set of ebit data for the nine months of the past two years is left out – hence to 9M 17, pre-Scharwath – would be depressing, but cherry-picking short periods (2012/2011; 2012/2010; 2012 & 2011/2009) where the growth rates were strong, should remind us that we are now in the third year of growth, which may or may not represent peak earnings/cash flow growth, but testifies to the likelihood that incrementally higher returns will be harder to achieve.

Given that, if the sleeping bear wakes up now, DHL GFF being accused of profiting from a great story to market to investors would be the lesser evil.

Another point is that its 3.1% underlying profitability, gauged by ebit/revenues (unadjusted), is back up a little closer to where a leading freight forwarder belongs (there are few public comparables, ex DSV PAN), but still only half way there judging by DSV PAN’s 6%-plus (some recurring items are never recurring with the old DSV, given how it deploys capital externally).

Add DHL GFF’s depreciation and amortisation of €65m quarterly, and its ebitda line in 2019 comes in at €724m.

Stamp on the division a multiple at no discount to DSV PAN’s skyrocketing valuation (~ 18 EV/ebitda; despite the latter’s stronger grow rate, higher margins, no overhang in terms of shareholding structure, yet a lowly yield), and the lightest unit in terms of assets in DP-DHL’s portfolio would be worth 13bn, excluding net debt considerations. (Short note for the reader: there remains a debt pile on the group’s balance sheet, see below – while for DHL GFF, a 2x net leverage in line with its parent might be acceptable) .

(Source DP-DHL)

A finance purist would tell you that a €13bn valuation (€14.5bn including net debt) is unfair, given the different prospects of the two, but the German company could become more appealing if it paid a significantly higher dividend rather than chasing M&A growth a la DSV (ex PAN) – it’s worth mentioning that DSV PAN is now worth €22bn on the stock market. And… the Danes trail at some distance in air, where DHL DFF is the global leader, and they are still 300,000 teu away from second-ranked DHL GFF in ocean; also, DHL Freight is much bigger than DSV Road, mainly where they both matter in Europe.

DP-DHL CFO Melanie Kreis knows how to ply her trade, and so does Tim Scharwath, while market consensus says CEO Frank Appel is pleased with both executive board members and with the way things are going business-wise. But group debt must come down. While Berlin rules on that front, they are all aware that DHL GFF monetisation is possible, as well as that DSV PAN’s success boils down to a lack of alternative choices for investors in the freight forwarding world, following the de-listings of PAN and Ceva in the past year.

{kind=link}