Private debt has become one of the hot topics for fund managers desperate to build a fee-rich asset class at a time when their traditional businesses are struggling. But even industry insiders are warning that the boom in private debt is turning into a frenzy.

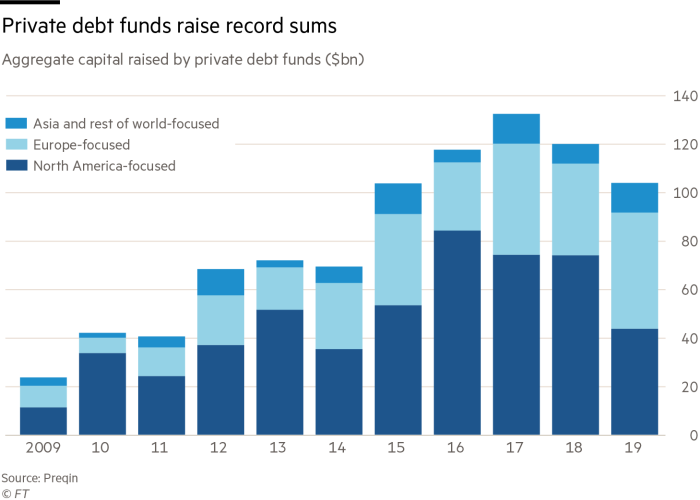

Once a niche area of the global asset management industry, assets invested in private debt — largely made up of non-bank loans to unlisted companies — reached a record $812bn in 2019, putting the market on track to break through the $1tn barrier within the next year.

The number of asset managers operating in the field also hit a new high last year, totalling 1,764, more than double the amount five years earlier, according to consultancy Preqin.

The main managers competing for assets were historically US private equity giants with credit arms, such as KKR and Blackstone. But more mainstream fund groups, including M&G, Schroders, Amundi and Standard Life Aberdeen, have made forays into the market in recent years, eager to take advantage of buoyant investor appetite.

Private debt is moving into the mainstream as investors hunt for higher yield. Its growth has been spurred by banks quitting the market when they rationalised their loan books to meet tougher capital rules.

“Sovereign wealth funds and large state pensions were among the earliest adopters, but increasingly the rest of the institutional investor world has followed suit,” says Ji-Eun Kim, head of private asset manager solutions at Schroders. “Private debt’s . . . enhanced cash yields are especially attractive in a low-return environment.”

However, a growing chorus of senior figures are voicing fears that the market is looking frothy as too much capital chases too few deals.

“It would be crazy to start a private debt business right now,” says a former senior private debt executive. Another senior private capital fund manager thinks the asset class is in bubble territory. “We see the same movie happen every time. When too much money goes into one place the outcome isn’t great.”

Vulnerabilities are already being exposed. In early February, Hadrian’s Wall Secured Investments, a listed fund that lent money to UK small and medium-sized companies, said it was winding down its business after warning of “material” losses on investments in two biomass companies.

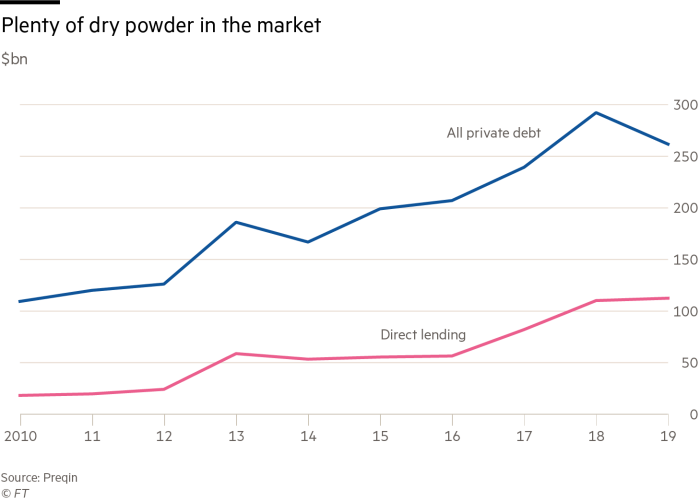

Preqin data show that over the past four years 327 direct lending funds, the most common type of private credit strategy, have been raised, with about $207bn flowing into the strategies.

At the same time dry powder — the amount raised for direct lending but not invested — is at a record $112bn.

Dry powder for all private credit, including strategies such as distressed and mezzanine debt in addition to direct lending, stands at $261bn, a figure that is down slightly on the year before but still represents the second-highest level on record.

The recent capital raising frenzy, combined with fierce competition among lenders, is damaging returns and loan condition standards are suffering.

Jaime Prieto, managing partner at Kartesia, an asset manager that lends to SMEs, says that some managers are yielding to pressures by agreeing to weaker loan terms and looser covenants.

“The huge amount of capital floating around means that it is inevitable there will be some deterioration in credit quality,” says the former senior executive. He says mounting leverage across private assets is evidence that problems are building up in a similar way as they did in the run-up to the subprime mortgage market crisis.

Mariano Belinky, chief executive of Santander Asset Management, which set up a private debt unit last year, says that more problems are coming down the track.

He highlights the recent spate of bumper fund launches as an area of concern. Last year a private debt fund managed by BlueBay Asset Management raised €6bn, while a vehicle from BNY Mellon subsidiary Alcentra closed at €5.5bn, nearly double its minimum target.

“How do you deploy that capital at scale?” he asks. “As the asset class keeps heating up, a lot of these managers will have a tougher time finding good deals.”

Other industry executives warn that the cracks now on show will become much worse when the market cycle turns.

Nicholas Brooks, head of investment research at Intermediate Capital Group, the £42.6bn specialist credit manager, says rising markets over the past decade have masked problems lurking under the surface. “There are probably a number of newer players that are lending unwisely but we won’t know until we get to the next downturn.”

There are also concerns that some fund groups have jumped on the private debt bandwagon without the skills to fully understand the risks of the loans they provide.

“As managers raise bigger funds, the question becomes can they originate big enough loans and do they have teams of experienced people to sort things out when problems arise,” says Paul Shea, co-founder of specialist SME loan manager Beechbrook.

Mr Belinky says Santander AM’s private debt unit, which benefits from access to its parent bank’s origination pipeline, has been approached by groups that are struggling to find deals by themselves.

“Managers have come in and said ‘Hey, we’ll buy 50 per cent of whatever you originate’. That gives you a sense of how managers have limited access to good deals.”

But Ken Kencel, chief executive of $21.5bn private debt house Churchill Asset Management, which examined 800 potential deals last year, takes a different view, arguing ample opportunities abound.

He says credit quality is holding up, particularly in the upper end of the market where fewer managers compete. Competition has long been most acute among managers looking to arrange loans for small and midsized companies.

Mr Kencel says that the groups that are able to write bigger cheques to corporates are still in a minority and will flourish in the coming years.

But writing big cheques is also risky, making it even more important for fund managers to have large teams of professionals tasked with monitoring the loans they have made.

Established private debt managers that benefit from revenue streams from existing funds can afford to finance this. But newcomers may take years before they turn a profit considering the high costs of arranging private loans and the fact that many groups earn management fees based on the amount of money they have invested, rather than raised.

Many believe the market is set for a wave of consolidation that will see smaller and less specialist groups squeezed out or merged with competitors. Investors are increasingly gravitating towards more established managers with larger funds; according to Preqin, the 10 biggest funds that closed last year accounted for 36 per cent of new capital raised.

Mr Belinky says that some managers are already conceding defeat. When his company was recruiting for a new private debt team last year, it received applications from professionals whose previous employer had been forced to close their private debt funds because they failed to find enough companies to loan to. “When we interviewed them, they said they had commitments from investors and were ready to go but just couldn’t find enough assets to put the capital to work,” he says.

In January, Swedish private equity firm EQT said it was considering offloading its €3.9bn credit arm to focus on its core business. M&A activity is already under way among specialist direct lending entities in the US known as business development companies or BDCs. Crescent Capital last year acquired Alcentra’s BDC, taking its investment portfolio to $923m in assets.

“In a more challenged credit environment, some of the smaller shops are going to find it hard to service their portfolio and have the resources needed to deal with restructuring their portfolios,” says Mr Kencel. “Rather than spending significant time working through these problems, some are likely to opt to sell.”

{kind=link}