The London-based International Maritime Organization (IMO) is hardly a household name. The IMO is a United Nations body responsible for the regulation of international shipping across the world’s seven seas. In addition to safety, maritime security, shipping efficiencies and legal oversight, the IMO remit includes environmental protection, a mandate that is expected to impose significant market reordering in the New Year. A 2016 decision to require the sulphur content of bunker fuel for the world’s 60,000 ocean-going commercial shipping fleet to fall from 3.5% to 0.5% promises to be both far-reaching and impactful on myriad market players. Those market players range from shippers to shipbuilders to ship owners to refiners to suppliers of crude oil – not to mention consumers – as the mandate unfolds in the New Year and beyond.

As with most far-reaching regulatory mandates, there will be winners and losers. US-listed shipping companies, such as Frontline (FRO), Nordic American Tankers (NAT), DHT Holdings (DHT) and Teekay Tankers (TNK) are currently on a tear as tighter capacity continues to exert sharp upward price pressure on freight rates for both tanker and bulk traffic. The shares of high complexity refiners with heavy-oil processing capability of the US Gulf Coast are also expected to benefit as demand shifts dramatically to low sulphur fuel oil (LSFO) mandated by IMO 2020.

The light, sweet crude produced in the US and many OPEC countries will, over time, command market premiums at the expense of high sulphur crude. At the same time, low-complexity refiners dependent upon imported gasoils will find such production inputs much more expensive. Heavy crude producers such as Venezuela, Canadian oil sands, high-sulphur crudes from the Middle East, Africa and beyond will find their production to be of lesser value on world markets.

Over time, the current price differential between US and Brent will likely flip as the demand for low-sulphur crude increases in global markets. Refining capacity adjusting to increased demand for LSFO could apply upward price pressure on other grades of refined crude products such as gasoline and jet fuel over the short and intermediate term. Alternative bunker fuels such as low sulphur diesel and liquid natural gas will also experience high levels of demand over time as fueling and production infrastructure come online to meet demand.

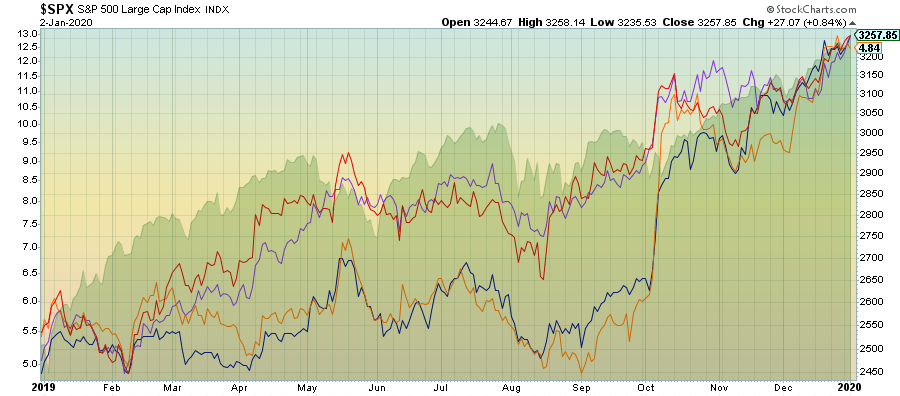

Figure 1: Frontline Ltd., Nordic American Lines, DHT Holdings and Teekay Tankers against the S&P 500

The fallout is already hitting markets. Frontline operates and/or leases 71 tankers that includes very large crude carriers (VLCC), Suezmax and Aframax through the end of September for a deadweight (DWT) average of 13.5 million (red line, Figure 1, above). Through the end of September, the company had 23 vessels under financial lease arrangements. Time charter equivalent (TCE) hit $28.97 million through the nine months through September, up 41% YoY. Voyage charter revenues hit $564.67 million, up 16% for the same period. Operating income hit $108 million, up fourfold YoY. Earnings per share hit $0.18/share, up rather significantly from the ($0.20) post YoY.

FRO has committed $9.6 million to equip 14 of its fleet with exhaust gas cleaning systems (EGCS), scrubbers for a per vessel cost of $685,714. In addition, the company contracted for an EGCS equipped VLCC and will take delivery of the vessel in May 2020. FRO also owns a 28.9% stake in Feen Marine Scrubbers, Inc. (FMSI) a leading manufacturer of EGCS systems. FRO has contracted with FMSI for 13 EGCS at $9.6 million or $738,461/vessel. FRO is up 126% on the year and 98% since the end of September. The S&P 500 (green area, Figure 1, above) was up just shy of 30% on the year.

Nordic American Tankers Ltd. (NAT) operates 23 Suezmax tankers which average approximately 156,000 dwt (orange line, Figure 1, above). In its latest SEC filing through September, NAT reports the strongest tanker market in decades, with TCE in the 3rd quarter at $15,900/day. This is a 7.4% increase over the $14,800/day post in the 2nd quarter and a 33% increase over the $12,000 YoY. The increase in TCE has driven total voyage revenue up to $32.35 million through the end of September, an increase of 15% YoY. The nine months through the end of September has voyage revenue at $116.6 million, up 46% YoY.

However, operating, general & administrative and depreciation expenses put operating income into the negative by $2.9 million for the quarter but rendered $10.5 million to the positive for the nine months through September. Earnings per share remain negative at the quarter ($0.10)/share, up a penny/share YoY and for the nine months ($0.16), up $0.44 for the period. Restricted cash deposits of $10.9 million was allotted through the end of September for future drydocking, with most of the sum going toward scrubber retrofits in the short and intermediate term. NAT is up 133% on the year and 159% since the end of September.

DHT Holdings (DHT) operates 27 very large crude carriers (VLCC) with an average dwt of 8.36 million. The company’s overall VLCC TCE earnings for the quarter through the end of September came to $25,500/day (purple line, Figure 1, above). VLCCs on time charter earned the equivalent of $33.700/day while the spot market was paying up to $61,700/day through the 4th quarter. Total revenues hit $104.7 million through the end of September, up 16.1% YoY.

The increase is due mainly to higher tanker rates, offset by an $8.3 million charge due to scrubber retrofits during the period. The company completed 8 of 16 exhaust gas cleaning systems (EGCS) during the period for a total cost per vessel of $1.03 million. The company’s net loss came to $9.4 million for the period or ($0.07)/share, up from an EPS loss of ($0.15)/share YoY. DHT is up 84% on the year and 49% since September.

Teekay Tankers (TNK) currently owns or leases 60 tankers, which includes 29 Suezmax, 17 Aframax, 9 LR2 product tankers and 3 support vessels. The company also owns a VLCC through a joint venture (blue line, Figure 1, above). The average TCE earnings for the company came to $18,992/day for the nine months through the end of September, a 31% increase YOY. Total revenues for the period came to $578.3 million, an increase of 17.2% YOY. Loss from operations came to ($149,000), up from a loss of $2.1 million YoY. EPS for the period came to ($0.08)/share, a ($0.16) improvement YoY. The company allotted $4.2 million for drydocking expenditures, mostly for the retrofitting of EGCS equipment. TNK is up 202% on the year and 194% since September.

Over the past several years, ocean-going tanker operators have reaped the benefits of fast-changing market conditions. US crude production is now at 12.8 million b/d through the end of November, an increase of 27.51% over production as recently as November 2017. US production has been available for export to the world at large only since the end of 2016. September marked the first month that the US was a net exporter of crude. With Venezuelan and Iranian export volumes already reduced by US sanctions, Gulf Coast ports are now handling an ever-increasing export volume, with much of that increase heading toward lucrative Asian markets. US crude exports averaged 2.9 million b/d in 2019, a 45% increase YoY. With new pipelines linking the Permian Basin with Gulf Coast ports, the US export volume in October was up to 3.4 million b/d. Add in an 8% price differential between the US and Brent pricing coupled with US sweet crude becomes a difficult deal to beat on most market measures.

Freight rates began to spike toward the end of September (see Figure 1, above) around a confluence of events. The Trump administration had just slapped sanctions on Chinese operated COSCO Energy Transport, one of the world’s largest tanker fleets with extensive operations in the Middle East, particularly in the shipment of Iranian oil to Chinese ports. China is one of Iran’s largest crude markets, having supplied about 6% of China’s total oil crude needs through the end of 2018, according to news reports.

The September sanctions drove daily tanker rates from about $18,000/day to $30,000 almost overnight. VLCC jumped to $78,000/day while the Aframax, a medium-sized crude tanker, hit $80,000/day. With increasing instability in the Middle East in the wake of the drone attack on the Saudi Abqaiq-Khurais oil facility in September and Friday’s US drone hit on Iran’s General Qassem Suliemani, tensions in the Middle East are close to the breaking point. US crude exports to the Pacific Rim has become an extremely profitable endeavor.

With the IMO 2020 mandate now online with the New Year, compliance now falls squarely on the shipper. Ocean-going vessels will be required to emit 85% less sulphur. Currently, about 75% of bunker fuel consumption is high sulphur fuel oil (HSFO). To meet the requirement, operators have four options: switch to compliant fuel oils that meet the new allowable standard of 0.5% sulphur emissions; install exhaust cleaning scrubbers to reduce the sulphur content or switch to alternative, low-sulphur fuel oils like diesel or liquid natural gas. Operators may also pay penalties. Each of these options have both advantages and disadvantages.

The switch to LSFO, of course, bestows immediate compliance. However, issues abound as to availability, specifications, compatibility – not to mention cost that could rise as much as 25%. On the availability, about 20 VLCCs are now moored off of Singapore filled with LSFO. The diversion of these vessels for storage purposes places even more upward price pressure on tanker rates. IMO 2020 has no enforcement power, placing compliance with local governments. The likely high cost or ready availability of LSFO could easily drive operators toward non-compliant fuel options. Many jurisdictions lack testing equipment to accurately assess the sulphur content of bunker fuel on board, while others still have yet to write IMO 2020 mandates into local law.

LSFO production is expected to increase from the current 1.4 million b/d to about 1.8 million b/d in 2020 as supply chains evolve. Currently, the ocean-going fleet consume about 3.5 million b/d of HSFO, posing gaping supply shortfalls at the outset as refiners gear up to meet new demand and fuel compatibility standards. Already an established fuel, marine diesel will likely be an early-on replacement for HSFO. That said, low sulphur diesel will also likely be the most expensive short-term option available.

Scrubber retrofits require up to a six-month lead time at considerable cost. During the 3rd quarter, about 9 million dwt of capacity was drydocked undergoing scrubber retrofits, which was one of the main drivers of rising tanker rates. Bulk shipper Maersk committed to scrubber retrofit orders totaling $439 million for 86 of its box ships, or about 15% of its 750-ship fleet. The retrofit works out to $5.1 million per ship. So-called open-loop scrubbers uses seawater to scrub down and remove sulphur deposits in smokestacks, flushing the resulting slurry back into the ocean. In-ocean disposal is itself of questionable environmental value and the practice is already banned in a growing number of global trading hubs including Singapore, China, as well as in California, Connecticut and Hawaii.

Currently, there are about 2,500 scrubbers that are on order or being fitted on about 1,700 ships, about 7% of the world’s total fleet through the end of 2020. The number of outfitted scrubbers is expected to rise to about 4,500 through the end of 2025. Of course, scrubbers theoretically allow shippers to continue the use of HSFO. Whether market forces will make allowance for the simultaneous production of both HSFO and LSFO over time remains a moot question indeed.

Liquefied natural gas (LNG) is a relative newcomer to bunker fuel. While compliant with IMO 2020, both availability and fueling infrastructure is currently limited. Further, LNG tanks take up considerable onboard space which could hinder the adoption of the technology. To date, there are about 100 LNG vessels in operation with a similar number that will come online in 2020. LNG vessels aren’t expected to power more than 10% of ships by 2040.

The refining of low sulphur diesel as a marine fuel is likely to reach about 3.3 million barrels/day through the end of 2020 – a six-fold increase since 2000. Refiners will have an incentive to tie into low sulphur feedstock for marine applications, increasing demand and price premium for sweet, low sulphur crude at the expense of sour, high sulphur crude.

Unsurprisingly, shipping companies have lobbied furiously for a delay in the implementation of IMO 2020. Many member states, including the US, have publicly indicated favor for delaying the ruling, particularly if shipping costs rise sharply that could further increase costs to the consumer and hence become yet another impediment to global economic growth. Bunker fuel prices have already risen about 20% since April 2018, prompting numerous industry attempts at protecting margins. Maersk announced an emergency bunker surcharge as early as May of 2018. COSCO, CMA, CGM and Hapag-Lloyd quickly followed suit. To date, there is no word on an implementation delay. And with tensions in the Middle East rising quickly, direction on freight rates coming from a distracted US administration is likely to be short on focus.

In the meantime, freight rates will continue to soar as IMO 2020 unfolds.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}