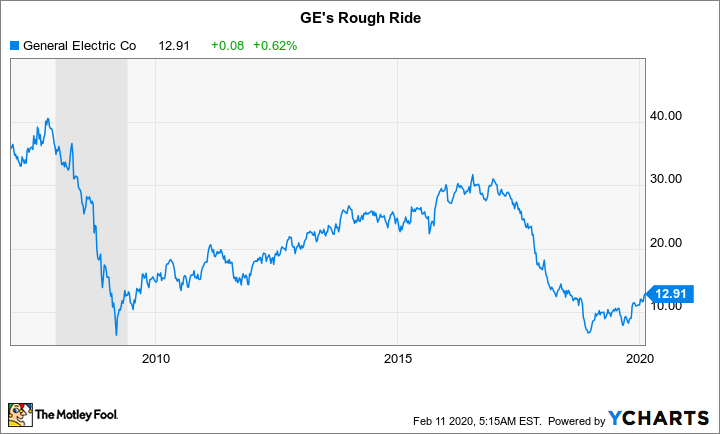

General Electric‘s (NYSE:GE) shares are up 40% over the past six months, with a 15% gain since the start of 2020. Backing up that price gain was a better-than-expected fourth-quarter earnings showing. Before you get sucked into the recovery story, though, step back and take a closer look at the bigger picture. Here are a few reasons most investors should remain on the sidelines at GE.

1. Debt is lower, but still a problem

One of the big underpinnings of GE’s stock advance was the company’s decision to sell a portion of its healthcare division. That move freed up around $20 billion of cash for debt reduction. Some industry watchers believe that this move, combined with other asset sales and cash-raising efforts, has basically solved the industrial company’s debt problems. This is wishful thinking.

Image source: Getty Images.

Even after reducing the company’s fourth-quarter debt load by $20 billion, debt still makes up roughly 70% of the company’s capital structure. That’s a significant number when you consider that peers like Emerson Electric and Honeywell are sitting at roughly 33% and 45% on this metric. This isn’t an apples-to-apples comparison because neither Emerson nor Honeywell have a financial arm like GE (more on this below), which is where more than 75% of GE’s debt lies. However, you can’t simply dismiss the leverage issue because GE’s industrial businesses and its finance arm all fall under the same corporate umbrella.

General Electric’s debt situation is much improved, but it still hasn’t fixed its balance sheet problems. And this doesn’t even take into consideration the company’s roughly $40 billion in insurance liabilities and annuity benefits (one of the bigger liabilities on the company’s balance sheet), which leads into concern No. 2.

2. The black box

One of the ongoing problems at General Electric is the company’s finance arm. This division was, basically, the one that brought the industrial giant down to earth during the deep 2007 to 2009 recession. GE started building its finance division under Jack Welch, and it expanded to the point that it had vastly outgrown its core purpose of helping customers buy the company’s products. There was no quick fix, but management did start to trim the division.

More than a decade after the recession ended, GE still hasn’t been able to extract itself from some of the troublesome finance-related businesses it got into. And worse, there’s no way for investors to really know what’s going on with the business. GE, meanwhile, has come out several times over the past decade and said that things were worse than expected in the finance division. This isn’t something that should inspire confidence.

To be fair, GE has made great strides in reducing the size of its finance business. However, at this point, what is left is likely a mixture of the core business (helping finance customer purchases) and the stuff GE couldn’t offload to others. That latter category is most likely the home of some really ugly things, noting that the “insurance liabilities and annuity benefits” liability on its balance sheet increased by nearly 12% in 2019.

That line item relates to insurance policies (such as long-term care insurance) that the company sold and is now allowing to run off. It must put money aside to pay for these liabilities, which is cash it can’t use for other purposes (see below for why that’s so important). These are very long-lived insurance policies, so this issue isn’t going away anytime soon.

The size of the finance issue is a big unknown for investors, and sometimes it seems that even GE doesn’t quite understand how big it is. The 12% increase in the “insurance liabilities and annuity benefits” line item was a tidy $4.2 billion. But that’s just chump change, noting that GE took an $11 billion charge in early 2018 with roughly 70% related to its insurance operations. It followed that up with an early 2019 announcement that it would need to take another $14 billion or so in charges over a roughly seven-year span to shore up its finance unit, again largely related to the insurance business. This is a complicated mess that will linger for years and that most investors would be better off avoiding.

3. Forward, at half speed

The next issue to keep in mind is that, even after GE solves the debt issue and fully mends its finance arm, it still has to run its main businesses. It’s doing a great job of that in its healthcare and aviation arms, where segment margins are robust, hitting 21.9% and 23%, respectively, in the fourth quarter. Healthcare threw off $2.5 billion in free cash flow in 2019, with aviation generating an even larger $4.4 billion.

General Electric’s problem is that its other two divisions, power and renewable energy, are struggling. Power’s segment margin was just 5.6% in the fourth quarter, with renewable energy posting a negative 4.1% segment margin. Through 2019, these two businesses produced negative cash flow of roughly $2.5 billion. GE is facing industrywide headwinds, so the troubles aren’t completely self-inflicted, but it still needs to fix these divisions if it wants to get back on the growth track. All in, they account for 40% of the company’s top line, so this is not a small problem.

A special situation

After a huge price decline, General Electric probably has material turnaround potential. But the turnaround, while making progress, still comes with notable risks. Most investors, particularly those with a conservative bent, should probably continue to avoid this industrial icon. Yes, GE was once considered a blue-chip stock, but it no longer deserves that moniker. And it’s likely to be a long time before it earns it again.

{kind=link}