To begin: ha! Hahahaha! Good lord!

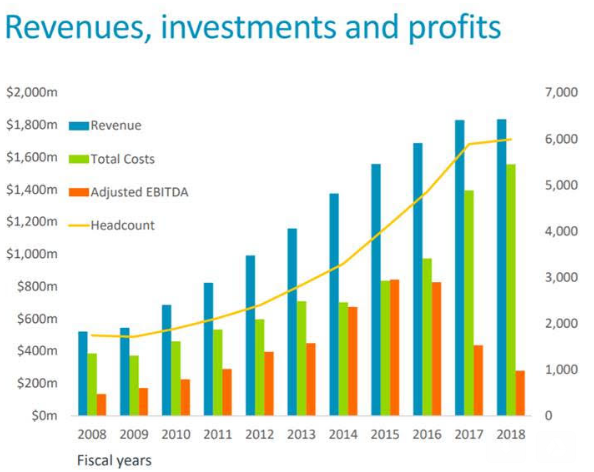

Elliott Management, the hedge fund, has built a stake worth $2.5bn in SoftBank and is pressing for a $20bn share buyback and governance changes at Masayoshi Son’s sprawling technology conglomerate, people with direct knowledge of the matter said.

Elliott, a $38bn US activist fund, wants SoftBank to narrow the discount between the value of its shares and that of its portfolio of holdings, which includes majority stakes in Sprint, the US telecoms group, and Arm, the UK chip designer.

It’s undeniable that the $100bn Vision Fund might be improved with better corporate governance, more transparency and tighter scrutiny of investment decisions — but the same is true of North Korea, and Elliott’s lobbying strategy has about as much hope of effecting change here as there. Mirabaud’s Neil Campling gives a good summary of the problem:

This, to us, looks like an investor using their status as a true activist and headline muscle to highlight the SOTP Trade more than anything else, particularly because activism in Japan is now far more difficult due to rule changes. SoftBank’s 26% stake in Alibaba alone is worth $152 billion. Throw in the Sprint stake and its Japanese mobile presence and the total already tops $210bn. That plus ARM, Boston Dynamics, Fortress Investment etc.

Arm Holdings (earnings chart above) and Sprint both look to have stagnated under Softbank’s control, Campling says. Any re-rating needs both a change of management culture and a multiple operational turnarounds, which will be a pretty big ask. He also highlights Japan’s Foreign Exchange & Foreign Trade Act, which came into effect in November and tightened all sorts of rules around foreign influence on national champions:

[W]hile there will be exemptions, foreign investors cannot propose the sale or transfer of business units at shareholder meetings, or place their own or related people on company boards – which is kind of central to the thesis of activists. The new regulations come into effect in May, just in time for the season of annual shareholder meetings in June.

It will be interesting to see if Elliott can enact change with Softbank management but the experience of another activist, Dan Loeb with Sony, suggests it will be a tough slog and have limited success.

So how far are we from Elliott itself being the sprawling, grandiose collection of disconnected minority investments that attracts the attention of an activist investor? Perhaps the next move is to attack itself.

Burberry’s has scrapped fiscal full-year guidance to no-one’s great surprise and shares are barely changed. The novel coronavirus has had a “material” effect on luxury foods demand in Mainland China, where 24 of Burberry’s 64 stores are closed and the rest are operating with reduced hours. Footfall’s said to be down significantly, including in Hong Kong (circa 25 percent of sales) and tourism spend will likely suffer in the coming weeks. Here’s UBS:

Burberry doesn’t quantify the impact on its FY2020 outlook (flat EBIT on FX-neutral basis). However, it states that its “most recent guidance for the year […] predates the impact of the coronavirus outbreak”. However, we estimate that a theoretical 20% drop in Chinese demand in one quarter could have a c7% negative impact on EPS, all else remaining equal.

Today’s release from Burberry confirms our view that the impact of the virus will be disproportionately more severe for the companies that are still in turnaround mode. Although we remain cautious on the sector near term, we retain our preference for LVMH, Kering and Hermès (all Buy rated), which we think are likely to be less impacted.

Tui, the holiday company that ruined The Strokes, has announced the sale of its Hapag-Lloyd Cruises into Tui Cruises, a joint venture with Royal Caribbean. The transaction is expected to close this summer. The €1.2bn valuation gives a dropthrough EV of 13.3 times ebita; pretty good, says Stifel, which had been using 11 times in its SOTP. More important though is the relief of balance sheet strain:

After years of ‘super normal’ capex growth to transform Tui from a tour operating-led business to a hotel/cruise content-led business, recent strategic priorities have centered around capital-light growth, particularly around digital initiatives. But ongoing disruption costs from the grounded MAX 737 aircraft have led to unwanted pressure on the balance sheet. We forecast 3.4x gross leverage in FY20 vs. TUI target range of 2.25x-3.0x. Selling HLC to the JV will bring in net cash of €700m, making a significant dent in the €2.1bn net debt we forecast at September 2020. TUI will only earn 50% of HLC’s profits which, in the short-term, will have a negative impact on the business mix. But TUI believes the new structure will provide a more flexible, capital-light way to growth the business. Our initial take is this is a sensible transaction to de-risk the balance and remove leverage concerns.

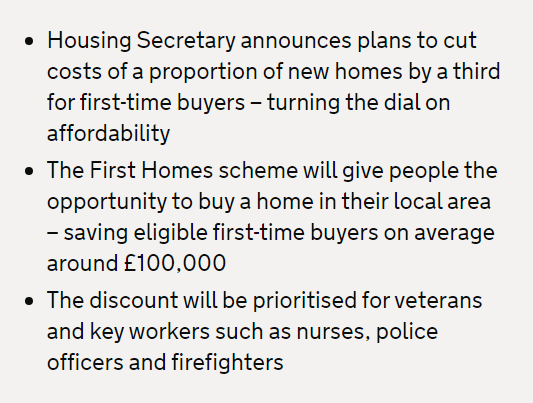

The Government’s having another fiddle with newbuild housing subsidies. This consultation, called First Homes, promises to “cut the cost of new homes by a third” with a “discount locked into the property to ensure more first-time buyers benefit in years to come”. The policy proposal was in the Tory manifesto so was well trailed and sector share prices have not budged:

The upshot here is that some plots on a site will be designated to be sold at a 30 per cent discount to first-time buyers, with the discount passed forward to subsequent buyers upon resale. This discount would be funded through homebuilder planning contributions, so “will not result in extra build costs” and will likely be offset by a reduced bung from affordable housing fund sources currently in place such as the Community Infrastructure Levy.

Will any of this deter the UK housebuilder cartel from earning absurd margins, strangling supply and flinging off cash? Almost definitely not, says UBS:

The impact on homebuilders will depend on the details, including the proportion of volumes dedicated to this scheme. If the scheme goes ahead and is funded by reducing other planning contributions, it should have no impact on returns. If it is additional to existing S106 contributions, site viabilities will change and the industry would either need to reflect this in lower land values (we think somewhat challenging given already low levels) or margins. We do not think there will be any short-term impact given (1) existing planning consents are unlikely to be affected and (2) the time it will take for any final conclusions to be reached. We therefore do not think the announcement warrants a negative reaction to the share prices, as appears to be the case. We have factored in a mid-term reduction in ROCE of approximately 500bps (from 24% in 2019) to reflect possibly less favourable Government incentives in the medium term (most notably Help-to-Buy, which is expiring in 2023).

Elsewhere in sellside, and Jefferies turns positive on Vodafone:

We upgrade Vodafone to Buy (from Hold). Our SOP-based Mar 2021 price target is 176p (previously Mar 2020 144p), offering 22% upside including dividend on a 1-year view. We show how tower monetisation can justify higher fair values in a range of approx 210p to 230p.

On the Organic Track, we believe Vodafone can achieve a 7.0% ROIC by Mar 2023 (from 5.1% in Mar 2020. Leverage falls to 2.7x (from 3.3x). Key building blocks are: managed recoveries in Spain and Italy, improving quality metrics in the UK and cost savings achieved ahead of peers being partially retained in rising margins. Our forecasts reflect the Egypt disposal announced last week, also NZ disposal and the acquisition of Liberty assets in Germany and CEE.

More interestingly, Jefferies puts a value on Vodafone’s country tower assets on between 16x and 24x Mar 2021 EV/EBITDA, or €16bn to €22bn. That would allow the release of cash proceeds of between €13bn and €16bn whilst retaining control, it says.

Our illustrative scenarios for tower monetisation reveal a Vodafone RumpCo offering a Mar 2021 ROIC of between 6.9% and 7.3%, and leverage of between 2.2x and 2.4x. Whereas Vodafone Group trades on 13.2x Mar 2021 EV/OpFCF, RumpCo is implicitly valued at between 11.5x and 12.2x. Sector average is 13.1x. We think that RumpCo would warrant a premium, reflecting its attractive ROIC and low leverage. Unlike sector incumbents it would not be expose to politically driven fibre build risk. Putting RumpCo on 15x suggests a Vodafone fair value of approx 210 to 230p.

Hurricane Energy, everyone’s favourite offshore Shetland complex geology punt, goes down to “equal weight” at Barclays post Thursday’s abandonment of the Lincoln-Crestal well.

2020 was supposed to when Hurricane provided the tangible data points needed to elevate the stock from a basement reservoir concept with niche investor appeal into an established UK oil production growth business. Instead the investment case appears to us trapped in its niche box: production data seems to be vindicating management’s development strategy, but the pathway to gradual medium-term cash flow and reserve growth upon which our Overweight rating was founded has stalled. The result is a stock that looks materially undervalued on paper (>50% discount to Tangible NAV, <$1/bbl of net 2P+2C); but lacks the catalysts needed to increase its appeal to a broader base of investors. We downgrade to Equal Weight with a new 22p price target (from 50p), which reflects our valuation of the developed 2P reserve base. We expect the 25 March Capital Markets Day to reiterate that the dream of large-scale West of Shetland basement reservoir developments is alive, but Hurricane’s path to achieving this has become increasingly unclear.

What else? Tidjane Thiam’s out at Credit Suisse. … Smart meter thing Calisen reopens the UK IPO market post Brexit with a midrange pricing. … Sirius-Anglo scheme’s published, revealing among other things that they considered for a $600m cash call. … Hargreaves’ Hargreaves takes £550m off the table. … And as a companion piece to the FT hacks’ guide to wellness earlier in the week, Simon Kuper has a very deep dive into the cause of and the solution to all of life’s problems.

What are we missing? Reader, do tell us below.

{kind=link}