Teekay Corporation (TK) flirted with too much leverage during the recent shipping downturn. Lately, shipping rates have become favorable which allows some extra income from exposure to spot rates. This has helped the company a little and provided a breather for the stock price. However, deleveraging will be in the future for a long time to come.

In theory, the holdings of partnership units in the subsidiaries should be marketable. However, Teekay did not handle the value of the Teekay Offshore units well because it sold the remaining Teekay Offshore (TOO) holdings for a very cheap price all at once with the IDR interest. That type of action concerns the market about the remaining liquid holdings because value is only what management receives for its liquid assets. This management needs to handle the financial challenges much better in the future. Hopefully, management will demonstrate that to the satisfaction of the market.

A far more conservative balance sheet strategy is called for. The last financial strategy cost the company any interest in Teekay Offshore. Cyclical companies always need to prepare for the worst possible outcome because sometimes that worst possible happens. Shipping is notoriously cyclical. Therefore, a countercyclical strategy of expanding during a downturn would provide the safety required for the limited partnership income strategy that is a major part of the Teekay organization.

Teekay LNG

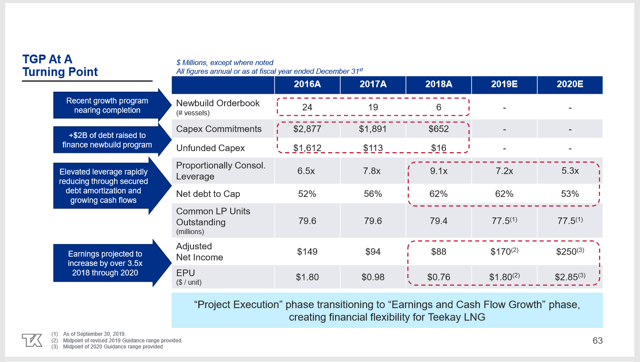

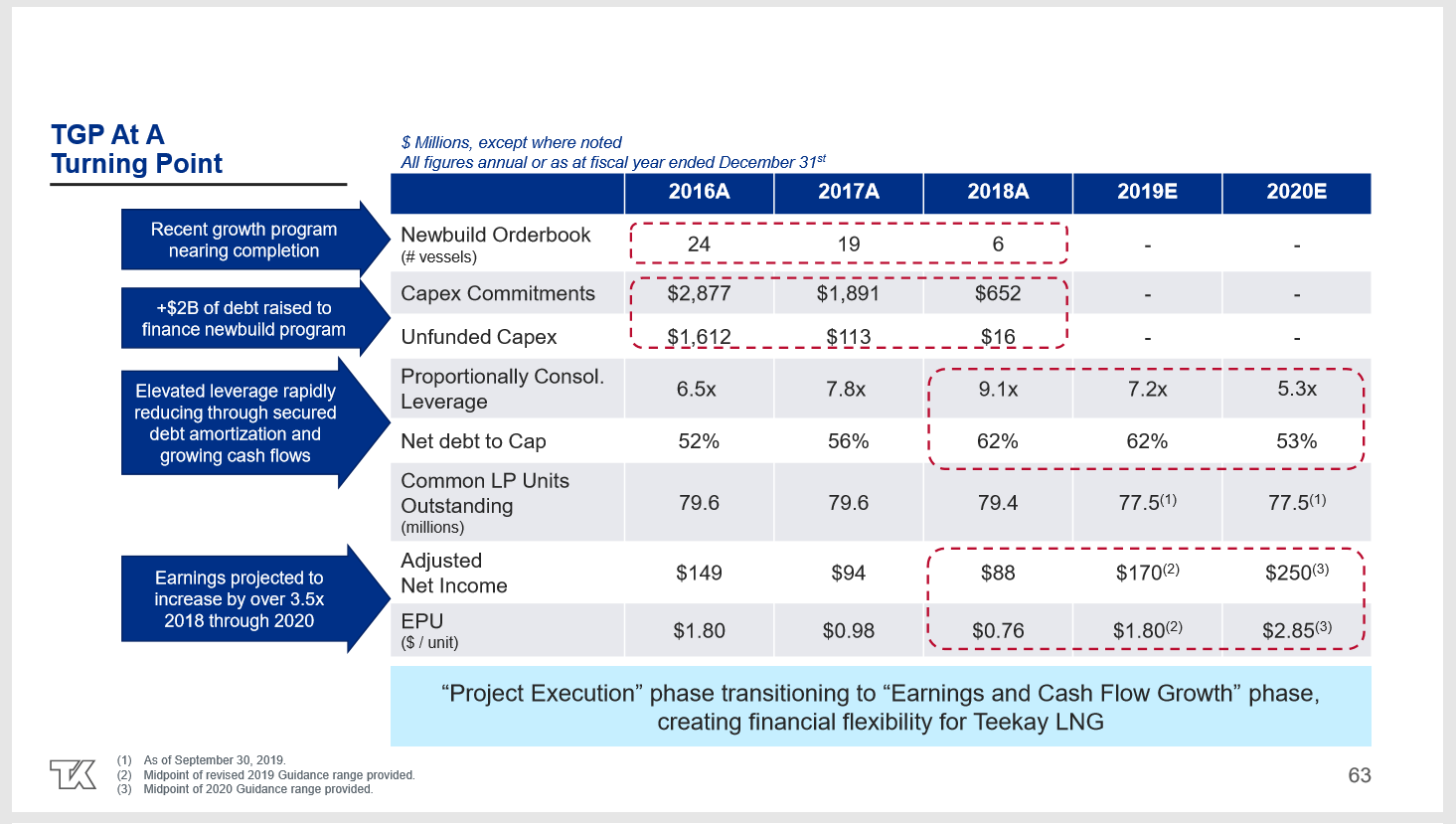

Teekay LNG Partners (TGP) has now accomplished a major expansion with the least amount of financial friction in the whole organization. Nonetheless, the leverage reached some eye-popping levels while the expansion program was underway.

Source Teekay Investor Day Slide Presentation November 2019.

The key here is to eventually get to ratios that will withstand (easily) the next shipping downturn. Teekay LNG has an advantage here with relatively long-term contracts that remain in force throughout the ups and downs of the industry cycles. However, the contracts that come due during a cyclical downturn will have to be renewed at a time of weak pricing. Therefore, the ratio goals shown above must be able to withstand that weaker pricing.

Management appears to understand this and has noted that deleveraging will be a priority for several years to come. There are some ships that are currently benefitting from decent spot market pricing. Shareholders need to have faith that management will choose an appropriate time to convert those ships to longer term contracts. The timing does not have to be exact, just reasonable.

Those investors interested in future income may want to consider these risky shares as a possible speculative part of the portfolio. The long-term contracts provide a reasonable and assured cash stream. Deleveraging appears relatively certain. Most of all as deleveraging occurs, there is a nearly certain dividend increase each year for the foreseeable future.

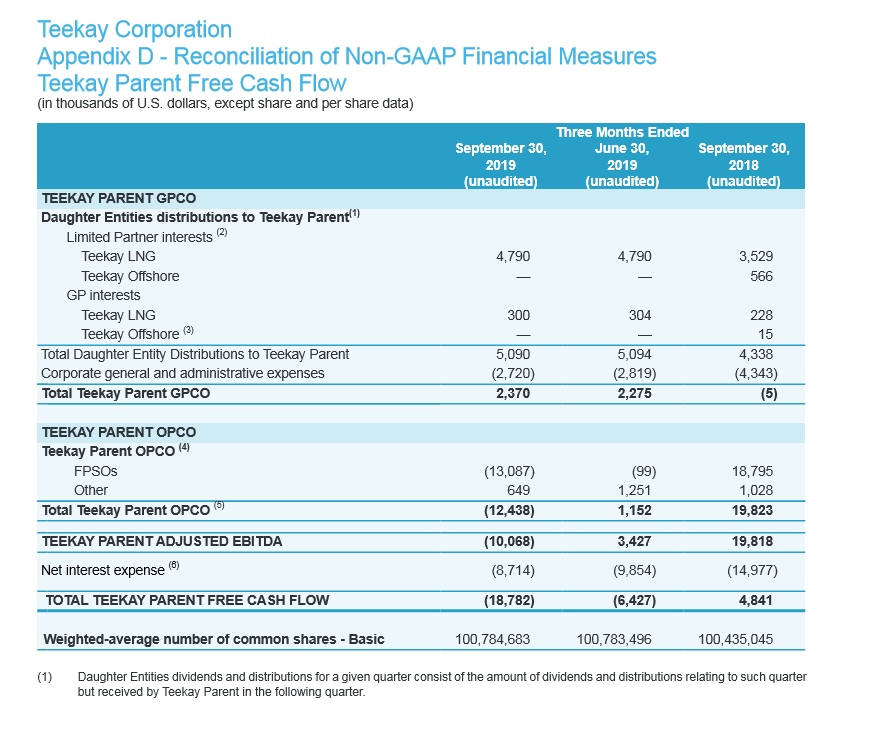

Effect On Teekay Parent

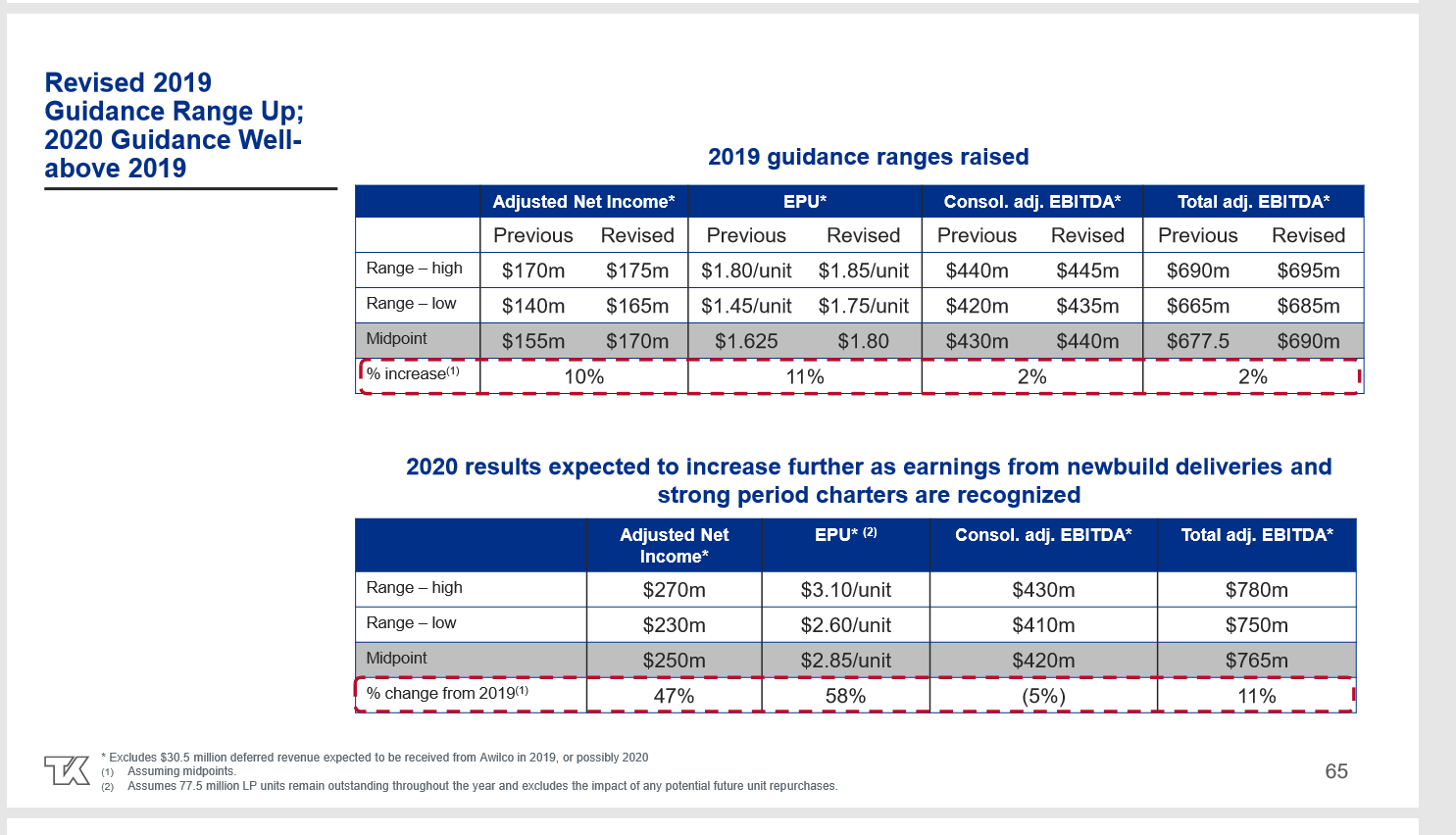

The mandatory debt repayments will limit the amount of money available for distributions. Therefore the strong market in the early stages is critical to a brighter future for Teekay to receive future income from the subsidiaries. The major effect on Teekay financial health will be from money received from Teekay LNG. So the increasing guidance shown below is very material to the health of Teekay.

Source: Teekay Investor Day Slide Presentation November 2019.

Teekay owns IDRs that enable Teekay to receive a portion of the income generated by Teekay LNG. Currently, those IDRs are not worth much because the income generated was far too low. Therefore, Teekay will wait to convert those IDRs to partnership shares sometime in the future when the income outlook is favorable.

In the meantime, Teekay received very little income from its interest in Teekay LNG for quite some time. Every time that Teekay LNG announces a dividend increase, the financial situation at Teekay becomes far more tenable.

Source: Teekay Corporation Third Quarter 2019, Financial Statements

The Teekay company income from its holdings in the subsidiary companies has been pretty low. There was a time when these holdings generated far more cash flow. Teekay LNG partners is expected to increase distributions by one-third (roughly). Teekay will benefit from this in two ways. Teekay will not only receive the increasing distributions, but it will also receive increasing income from the GP interests.

This increase is very important because the parent company only receives the cash shown above.

Source: Teekay Corporation Third Quarter 2019, Financial Statements

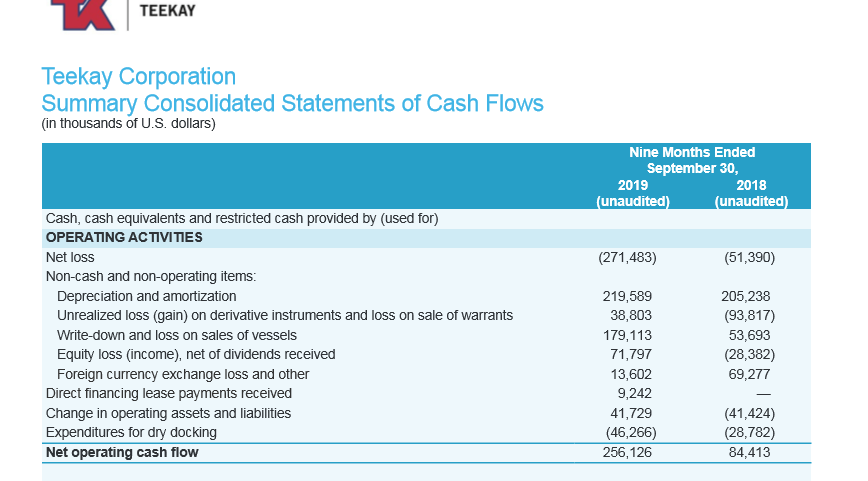

For a long time, management has pointed to consolidated cash flow to assure shareholders that everything is fine. However, the deleveraging obligations meant that no subsidiary had extra money to send to the parent company. Therefore, the only cash flow available to Teekay was the parent level cash flow, not the consolidated.

This led to some problems because as shown in the first earnings slide, the parent company really had no cash flow. Therefore, if a subsidiary got into financial trouble, Teekay had financial guarantees at the time it was in no position to honor, let alone solve the financial problems of a troubled subsidiary. That situation led to the complete loss of the financial interest in Teekay Offshore.

Source: Teekay Corporation Third Quarter 2019, Financial Statements

Even now, the parent company clearly must use some of its cash balance to meet the day-to-day operations. Not every quarter will generate cash flow to the parent company after expenses. Therefore the currently strong shipping market with the generous spot pricing allows the subsidiaries to delever a little bit faster. That means more generous distribution (or dividend) increases in the future. Therefore, the parent company cash flow will be adequate sooner.

The proper servicing of the parent company debt shown above as well as a reserve buildup for the next downturn probably would entail an annual cash flow in excess of $100 million to the parent company. That will more than likely happen in the future. The first step is for the subsidiaries to increase distributions enough so that Teekay no longer must use its cash balance.

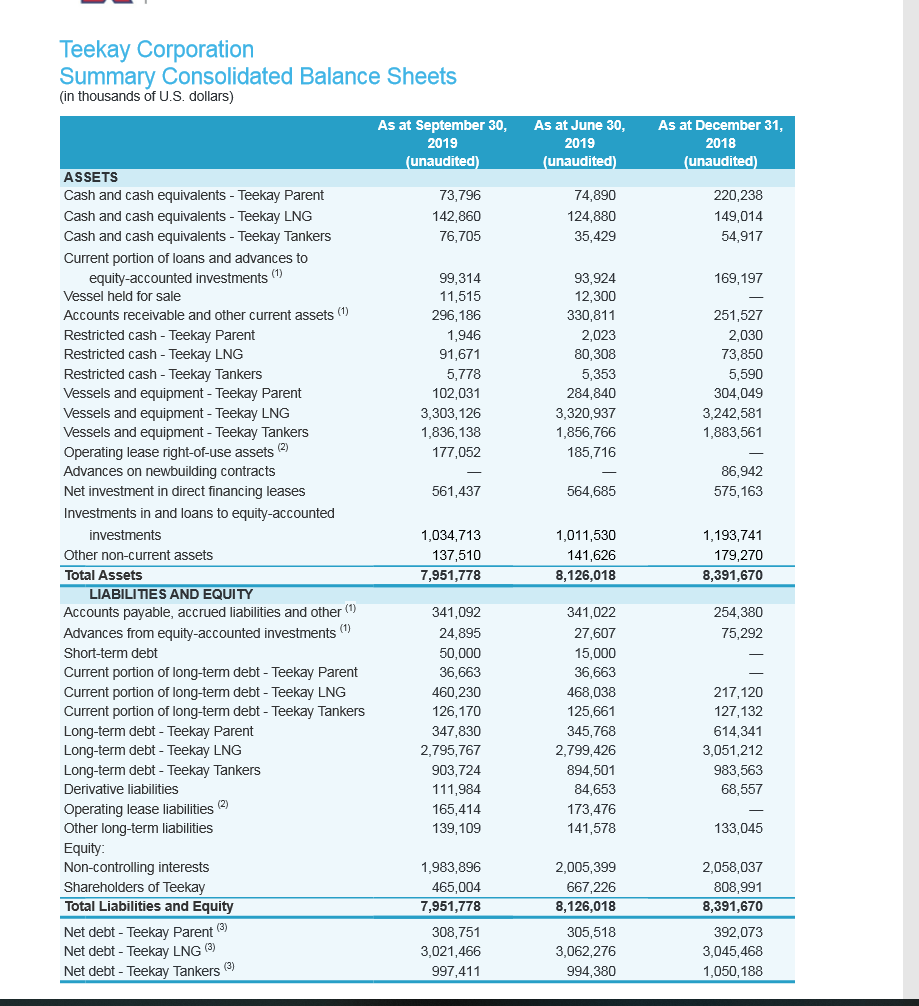

Teekay Tankers (TNK) is far more exposed to income variability and therefore needs to delever much faster. It is, therefore, unlikely to contribute to the parent company income stream for a while.

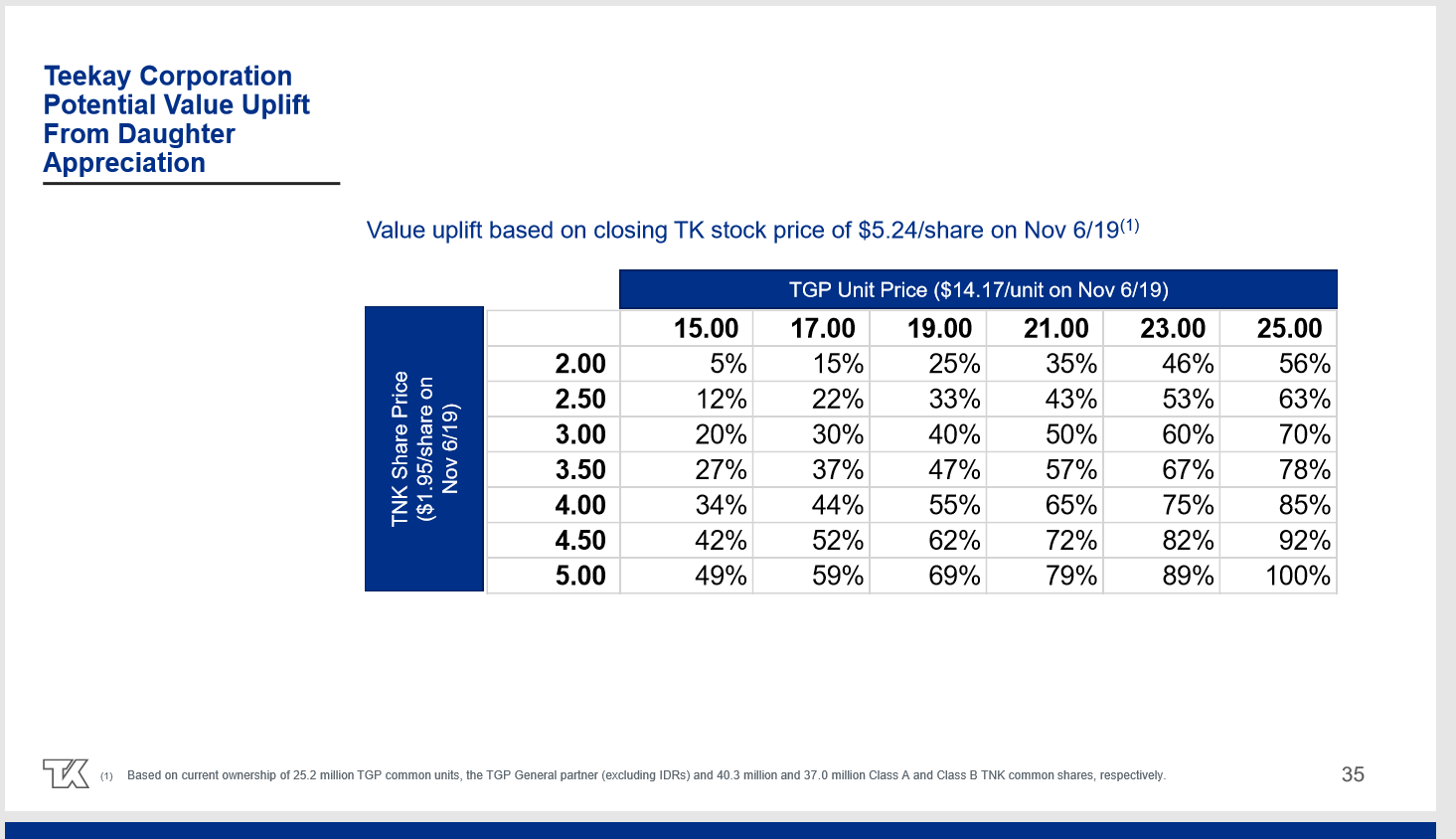

The Future

Teekay cost itself a lot of goodwill when it came to the market with a share offering and convertible debt that surprised the market. Therefore, the current price is not surprising. All of the management talk about asset values and future values carries no weight if management is going to sell stock unexpectedly to fix potential liquidity challenges.

Source Teekay Investor Day Slide Presentation November 2019.

The values shown above are contingent upon reasonable rates for the contracts outstanding as they come up for renewal (which is likely) as well as a lack of common share offerings in the future. The risk is still that Teekay will need external financing until the parent company level cash flow becomes adequate to service the parent company debt.

Management may elect to sell the ships owned by the parent company to pay down debt. That would certainly add a lot of clarity to the parent company’s situation in the eyes of the market. In the meantime, the anticipated stronger income from both subsidiaries combined with the anticipated Teekay LNG distribution increase should help the parent company cash flow situation and the market-anticipated future cash flows materially. It will probably take a few years before the unconsolidated parent company cash flow rates become acceptable to most lending guidelines.

Therefore, there is some risk here to income investors. This issue is not for the fainthearted or conservative investor. But that risk level has an excellent chance of predictably decreasing every year. Since both subsidiaries are now in the early stages of a cyclical recovery, this speculative issue should treat shareholders well over the next five years.

Despite a lot of intentions to the contrary, oil and gas along with the necessary services provided by this company will be around for a very long time. Therefore, this company has a bright future. It is definitely a variable income entity. Distributions will be great at cyclical highs and low or non-existent during industry low points in the cycle. Mitigating those future cycles through better financing and less ambitious growth plans will be the challenge. Ideally, there should be enough long-term contracts at the subsidiaries to thoroughly insulate the parent company from the industry highs and lows. But that has not worked out well in the past. Teekay Tankers has the most exposure to spot prices while Teekay LNG has the least. Therefore, the time to consider an investment in Teekay is at the industry low point until the recovery gains traction.

I analyze oil and gas companies and related companies like Teekay in my service, Oil & Gas Value Research, where I look for undervalued names in the oil and gas space. I break down everything you need to know about these companies – the balance sheet, competitive position and development prospects. This article is an example of what I do. But for Oil & Gas Value Research members, they get it first and they get analysis on some companies that is not published on the free site. Interested? Sign up here for a free two-week trial.

Disclosure: I am/we are long TK. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}